- Follow us:

- Our Commodities:

-

Leaf services published their final notice in the Government Gazette of their intention to inspect the grading of grain and oilseeds at a cost of R1.80 per ton. According to the notice, Leaf intended to implement on 12 July 2021. Grain SA, together with other roleplayers in the industry are represented by a highly respected law firm, to appeal against the final notice and retract the Leaf Services proposal. Litigation will be considered if needed.

Grain SA wants to notify members that certain inputs, especially inputs imported with cargo ship containers, may experience temporary shortages. It is especially agricultural machinery and agricultural chemicals (see full insert in Newsletter) that are affected by this. It is recommended that members start with input planning earlier this season. The lead time (time from order to delivery), can now be much longer than usual during restrictions.

Grain SA and the Directorate of Climate Change and Disaster Management is fostering collaboration. Industry gave feedback on its progress in the Quelea project with the aim to “Improve management of Quelea populations in South Africa”. Positive feedback was received and mention was made of the Department’s challenges experienced with locust in the Free State which should be closely monitored in the season to come.

The issues with maize cooking quality experienced last year were discussed with stakeholders in industry. The SAGL will be conducting a project on this matter over the next year.

A sorghum cultivar trial site visit was held between Mthata and Ugie during June. All seed companies are collaborating for the first time on a cultivar trial site in the Eastern Cape. The site visit was well attended by various role players ranging from small-scale to commercial producers, seed companies, Dannhauser Malt, and the Department of Agriculture, to name a few. The performance of the sorghum looks promising although the market remain a challenge.

As required by our members, there have been many negotiations since 2019 regarding the adjustment of grading regulations. Grain SA has ensured that the necessary mandates are obtained continuously at regional meetings, Congress as well as the Maize Working Group. The purpose of the changes was to ensure more transparent grading, ensuring definitions still apply and to eliminate subjectivity as far as possible. It was very important that the grading changes did not harm exports.

Changing grading regulations is a difficult process that involves a lot of negotiation. It is extremely important that if significant changes occur, they must be based on scientific evidence. Attempts are also made to reach consensus within the industry on changes, thus facilitating the process going forward and because it is important that producers and buyers/consumers take each other into consideration. Among others, the South African Grain Laboratory (SAGL) plays a very big role and their annual quality reports funded by the Maize Trust are extremely important.

The entire grading system has been reviewed. A summary of the most important proposed changes are

Frost damaged kernels

The definition of "ripe damaged kernels" was not sufficient with many differences within the industry regarding its citing. It was very important that a grader not only relied on experience but that the definition gave him the necessary guidance to make a consistent decision. The role players within the industry, together with independent experts, decided on the following:

Frost damaged kernels: means maize kernels damaged by frost; characterised by two or more of the following; a) a dull brown discoloration from the point of attachment b) an underdeveloped endosperm relative to the germ; and/or c) the pericarp has blisters or is flaky if there are signs of frost damage.

Defective kernels

In terms of defective kernels it was agreed to replace the description of mildew (mouldy) with fungus infected kernels. Fungus infected kernels therefore mean the following; a) are characterised by black, blue, green, yellow or white fungi growing everywhere on the kernel, or are characterised by fungi below the bran layer of the kernel; b) is infected by head rot and is characterised by red, pink or brown discolorations. The seeds are partially to completely infected. It was also decided to remove the herbaceous definition. It was further decided to not classify oxidation and pink maize as defective kernels.

Grain SA felt that these kernels did not have a significant impact on quality. Accordingly, the SAGL was requested to investigate, and determine the impact on the quality characteristics. The study was funded by the Maize Trust. Obtaining samples of purely discoloured and purely water-damaged kernels were initially a challenge for the SAGL. Many of the samples contained a combination of frost damage that would not provide the correct results. Grain SA and Agri businesses supported the SAGL to obtain sufficient quantities of samples. The SAGL conducted the study with the conclusion that these two factors in isolation do not have a significant impact on quality. The industry consequently decided to remove it as defective kernels as it causes grey areas in the grading regulation and should not be considered as defective kernels. It was decided to keep the definition within the grading in order to support the grader in the identification and to classify it as non-defective kernels. The changes will provide a lot of support in terms of subjectivity.

Research around hectolitre mass and stress cracks was done. The conclusion was that although there is a correlation with quality characteristics, it will be extremely difficult to link all the grading classifications to a precise figure and implement it in practice. Grain SA was also very concerned that it would cause double penalties if all the other classifications were still in place.

Part of the negotiation was the view of role players that a cultivar list and hectolitre mass should play a role. Grain SA and some of the other role players strongly opposed this with the opinion that the producer should have the freedom to determine for himself which cultivars are profitable and that the seed company already conduct many tests on quality to ensure that their products fall within the quality parameters.

It was agreed, however, that within a second phase of grading changes, a super grade could be investigated. The super grade must then earn a %-premium above a Grade 1 white maize and will be subject to specific characteristics and cultivars. The normal grading system therefore still remains in place. Many questions regarding practical feasibility and research have arisen from this and a task team has been set up to investigate the proposal and submit concrete evidence and proposals to the Forum. The action will therefore be evaluated and discussed in a second phase of grading change.

Several questions have been raised about the use of automated systems to eliminate subjectivity and the impact of the grader, similar to the citrus industry. South Africa is very unique in terms of its grading requirements - specifically in terms of white maize. International systems and algorithms have already been tested at the SAGL but given the results and costs, no successful system has been found to date. The possibility of future developments, however, has not been ruled out.

The changes were thoroughly discussed over a period of two years and researched within the Maize Forum on the basis of scientific evidence. Many proposals that would negatively affect producers could thus be repelled. All the role players consulted with their members and a final proposal was approved by the Forum’s steering committee. The proposals for change are now being sent by the Maize Forum to the Department of Agriculture, Land Reform and Rural Development, after which the department will review the changes and publish them in the Government Gazette for comment. After comments are received, they are sent to the World Trade Organisation for comment. If there is no opposition, the Minister of Agriculture, Land Reform and Rural Development can approve it, after which it will be promulgated in the Government Gazette.

Grain SA together with Johann Strauss from the University of the Free State held several workshops with the JSE to discuss the new methodology. Grain SA is happy to report that good progress has been made. At the recent workshop the following decisions were made:

Although Johann Strauss is currently doing his PhD study on maize, everyone felt that it would be easier to do the test on soybeans. The reason being that soybeans do not yet have a full differential system and that the market is smaller. The JSE did however, as indicated in earlier communication, indicate that if the system appears to be working, it will also consider rolling it out to other crops.

In short and as regularly communicated, the model determines the differential given the actual flow of grain in the system. Thus it accounts for supply and demand as well as locality competition. This means that localities that are within an oversupply area have a calculated local differential and localities where there is a balance of supply and demand have no differential.

Johann Strauss' research has shown that it limits revivals and also offers the opportunity to have a zero differential at favourable localities. The advantage is the differentials are calculated as close to the actual flow of grain, as possible.

For more information you can consult the following links:

South Africa relies on imports to meet the local input needs, which places the local agricultural industry at risk regarding availability and prices from the source countries. South Africa's sophisticated and organised input industries have always managed to avert critical input shortages, failing which could have caused food security problems in the country. Since March 2020, when COVID-19 restrictions began across the world to curb the pandemic, input availability has been disrupted, which also has implications on the price.

Availability of agricultural chemicals (especially glyphosate)

The restrictions disrupted raw material production in China earlier in 2020, while floods aggravated things in August and glyphosate manufacturing came to a halt during the repair work on 2 different plants, that manufacture 65% of china’s glyphosate production. In February 2021, there was the so-called “big freeze” in Texas USA, which negatively affected the availability of raw materials and additives. Interruptions in logistics greatly influence the flow of agricultural chemicals, for instance, the Suez Canal and especially the transport of shipping containers. Oxygen is required in the production of glyphosate; however, at this point, it is prioritised for the Covid-19 patients.

It is important to remember that due to the 100% reliance of South Africa on imported agricultural chemicals, logistics play a big role in availability. Before, the pandemic lead time (from placing an order to delivery) was 8 to 12 weeks and according to companies, the current lead time is about five months. The availability of shipping containers in the right places is a challenge in international trade at the moment. Due to China's quick economic recovery, after Covid compared to other countries, for every three cargo containers leaving China, only one returned with goods. Many containers must therefore return empty, which increases the cost of shipping. All these developments have critical implications for the availability of agricultural chemicals and on a producers' planning for the coming summer grain season. The likelihood is that South Africa will not obtain all its glyphosate needs. With the logistical challenges, other products may also be delayed.

Prices of international agrochemicals

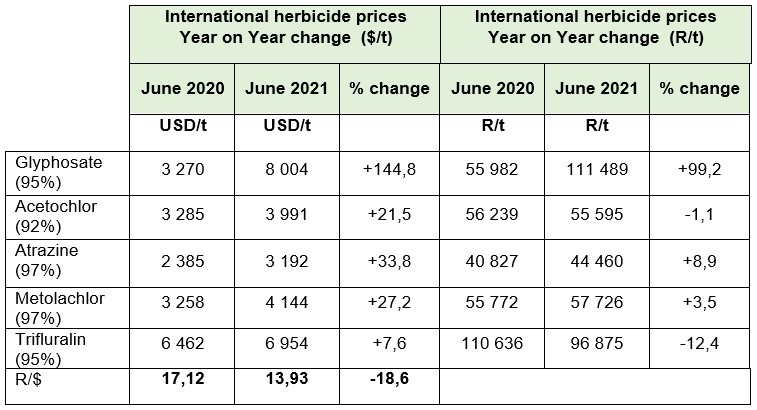

Table 1 indicates international herbicide prices (in a Chinese port) per active ingredient over a year. The left depict the prices in Dollar terms and the right depict the same prices converted into Rand value. It is clear that all herbicides have increased in Dollar terms, with Glyphosate and Atrazine taking the lead at 145% and 33.8% respectively followed by Metolachlor 27%, Acetochlor 22% and last Trifluralin with 8%. Prices in Rand terms followed a similar upward trend except for Acetochlor and Trifluralin , decreasing moderately. However, the increase in Rand terms did not increase in equal or greater proportions as can be fundamentally expected due to the support of a stronger Rand.

Table 1: Yearly herbicide prices: International in Dollar and Rand value

Source: Grain SA

Source: Grain SA

*Data as at July 2021

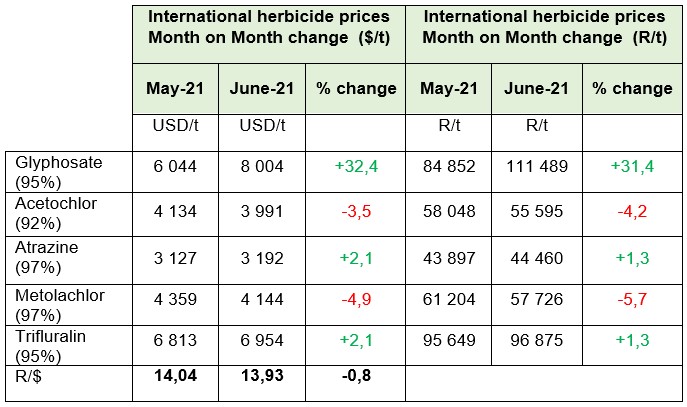

Monthly herbicide prices between May and June 2021 (table 4) indicate a decrease in some prices, while others are increasing in Dollar- and Rand terms. Both price trends are moving in the same direction. The most significant increase is seen in Glyphosate, with 32.4% in Dollar terms and a 31.4% increase in Rand terms. The slightly lower increases or decreases in Rand terms are attributed to a stronger Rand.

Table 2: Monthly herbicide prices: International in Dollar and Rand value

Source: Grain SA

Source: Grain SA

*Data as at July 2021

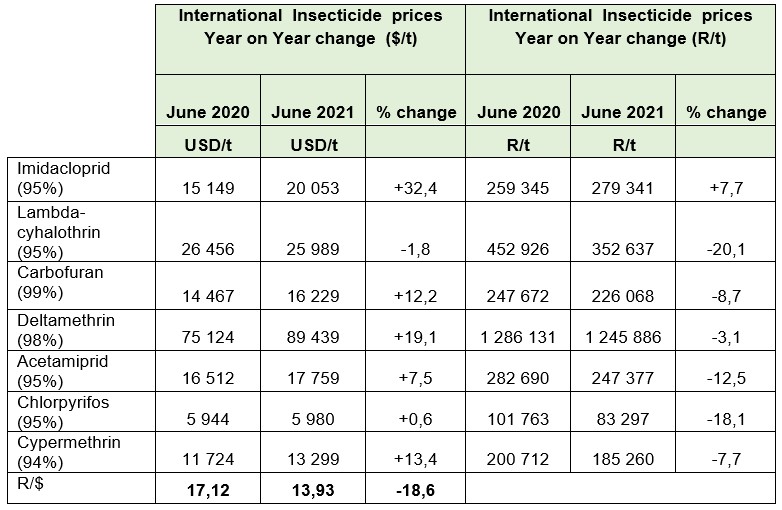

Table 3 indicate international insecticide prices per active ingredient over a year. The left indicate prices in Dollar terms and the right is the same prices in Rand value. In Dollar terms, all insecticides have increased except for Lambda-cyhalothrin, which decreased by 1.8% in a year. However, due to the strengthening of the Rand, most active ingredients decreased, except for Imidacloprid that shows a moderate increase of 7% over a year.

Table 3: Yearly insecticide prices: International in Dollar and Rand value

Source: Grain SA

Source: Grain SA

*Data as at July 2021

On a monthly basis, international insecticide prices (table 4) also show increases for most of the insecticides in both Dollar and Rand terms except Chlorpyrifos which decreased by 0.5% in Dollar terms and 1.2% in Rand terms.

Table 4: Monthly insecticide prices: International in Dollar and Rand value

Source: Grain SA

Source: Grain SA

*Data as at July 2021

Conclusion

This information must not lead to panic buying; this will only aggravate the situation. Producers are advised to contact their representatives to ensure that sufficient agrochemicals are available for the planned plantings in the 2021/22 season. If necessary, consider alternative remedies where, for example, there may not be enough Glyphosate available. Because the lead-time in the Covid period is so much longer, input planning for the coming season should be done earlier than usual.

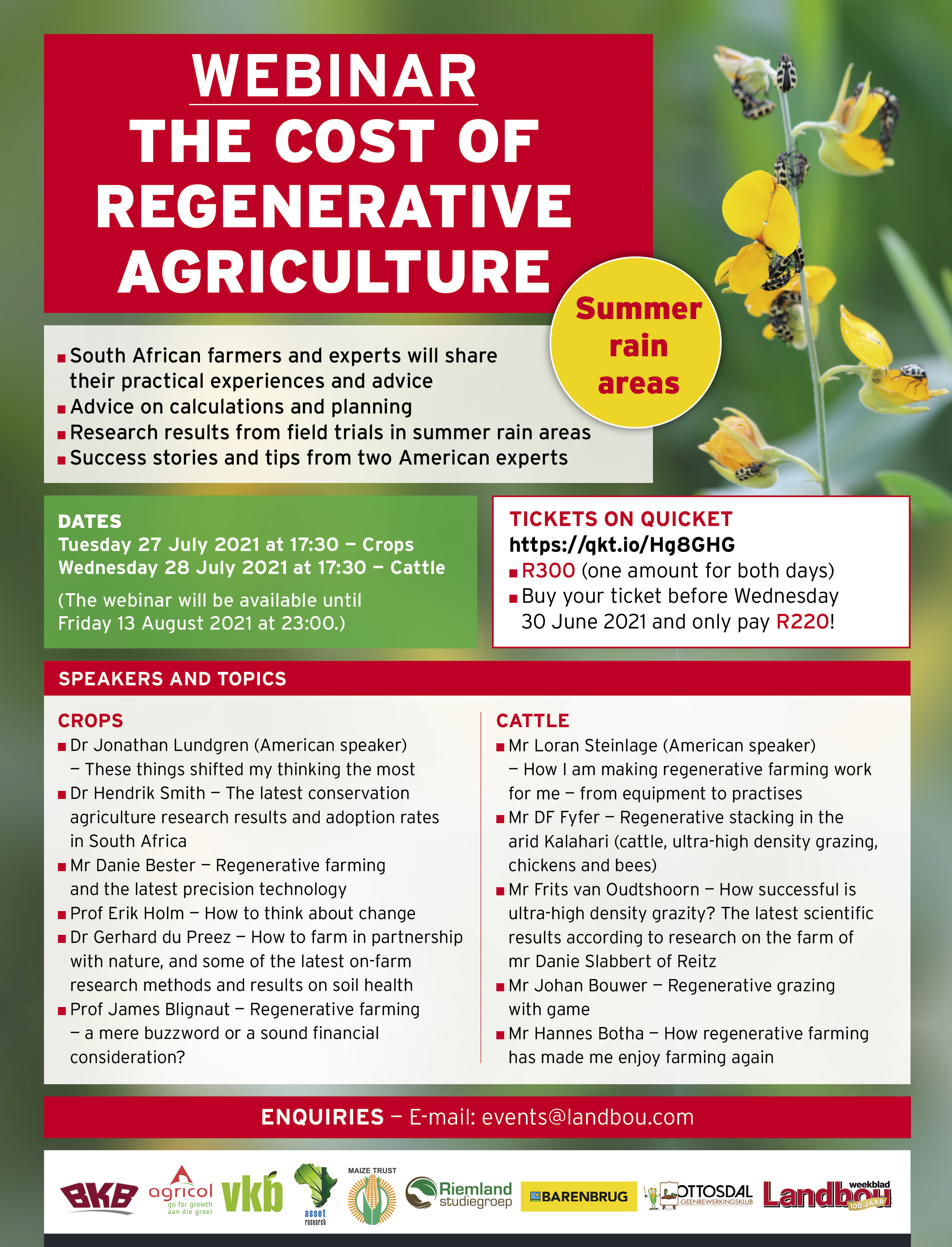

Producers are invited to a webinar discussing the cost of regenerative agriculture. South African farmers and experts will share their practical experiences and advice , offer advice on calculations and planning, share research results from field trials in summer rain areas, and share success stories and tips from two American experts.

DATES:

Tuesday 27 July 2021 at 17:30 — Crops

Wednesday, 28 July 2021 at 17:30 — Cattle

(The webinar will be available until Friday 13 August 2021 at 23:00)

For the full list of speakers and topics and for ticket details, click on the link below: