- Follow us:

- Our Commodities:

-

July 2020

| Ikageng Maluleke, Agricultural Economist, Grain SA. Send an email to Ikageng@grainsa.co.za |

|

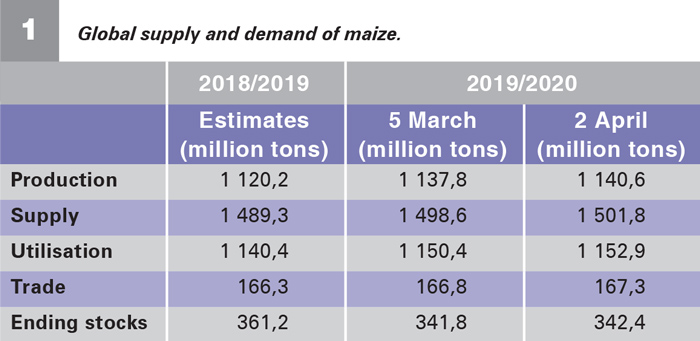

Global maize production has been raised slightly due to an upward revision in harvested area and yield for the European Union.

Utilisation for 2019/2020 is expected to marginally increase by 1% compared to the previous season due to the upward revision in the European Union and Russia. Compared to the previous season trade forecast for 2019/2020 (July/June) has increased marginally to just over 167 million tons, which is at a record, supported by ample export supplies. Ending stocks for 2020 remain almost unchanged from March, but still expected to decrease by about 5% compared to the previous season.

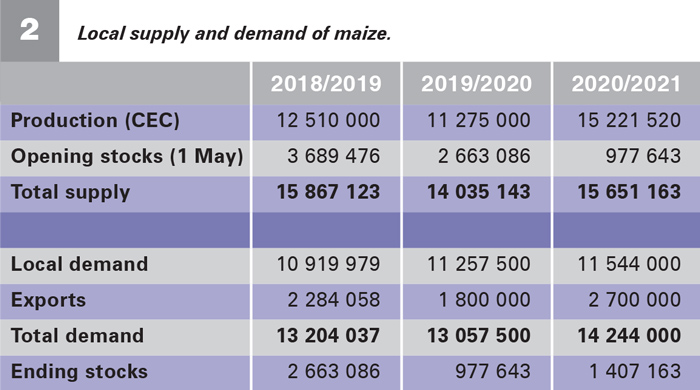

According to the crop estimates committee, maize production is forecast at 15 221 520 tons, with 8 779 470 of white maize and 6 442 050 tons of yellow maize. This a 2,78% increase compared to the previous forecast and 35% increase compared to the previous season. The expected yield for white maize is 5,43 t/ha, while the yield for yellow maize is expected to be 6,48 t/ha.

Local demand for maize is expected to increase by about 2,5%, mainly due to the increase in animal feed and human consumption. Due to the increase in production, it is to be expected that maize imports will be kept minimal, while imports will increase compared to the past two seasons and this is mainly for whole maize.

The export outlook for 2020/2021 is further supported by the sharp depreciation of the rand since the COVID-19 pandemic hit the South African shores. The low value of the rand has increased the competitiveness of South African maize on the international market. The depreciation is also expected to spur a rise in exports of yellow maize, which declined to a below-average level of 400 000 tonnes in 2019/2020. Ending stocks are expected to be about 43% higher than the previous season, this would be

enough to last about one and a half months if 940 000 tons is processed monthly.

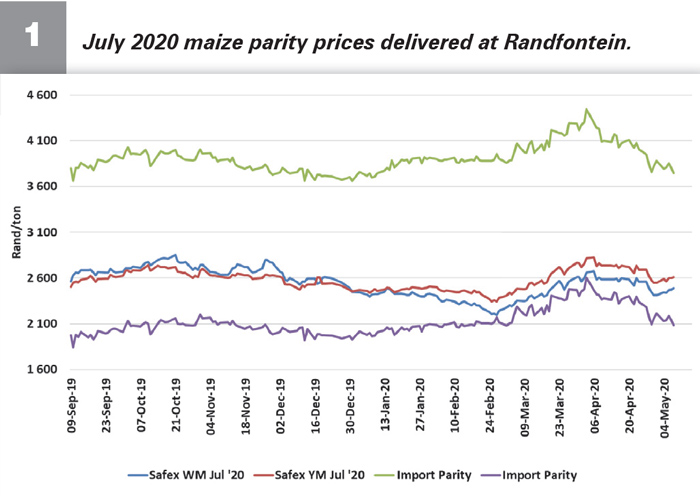

White maize prices increased by 7% in March 2020 and 24% in April compared to the same period in 2019, following the sharp depreciation of the rand together with strong export demand, mainly from Zimbabwe. At the March level, the price of yellow maize was at a comparable level year on year, while it increased by 8% in April. Both white and yellow maize July futures prices have followed the sentiments of higher prices and are trading at export parity levels (Graph 1).

Source: Grain SA, 2020

Source: Grain SA, 2020

Source: USDA, 2020

Source: USDA, 2020

Source: NAMC and Grain SA, 2020

Source: NAMC and Grain SA, 2020

Publication: July 2020

Section: Pula/Imvula