- Follow us:

- Our Commodities:

-

August 2014

WANDILE SIHLOBO, economist, Industry Services, Grain SA

South Africa’s 2014/2015 maize export pace have been slow relative to last year’s pace; on 18 June 2014 total exports were 60% behind last year (at 139 313 tons, compared to 345 019 tons in 2013/2014).

There are a number of factors resulting in this slow pace, but one notably being the soft demand in traditional South African export markets. Thus, this article aims to view the South African export market structures, as well as the possible export opportunities in East Africa.

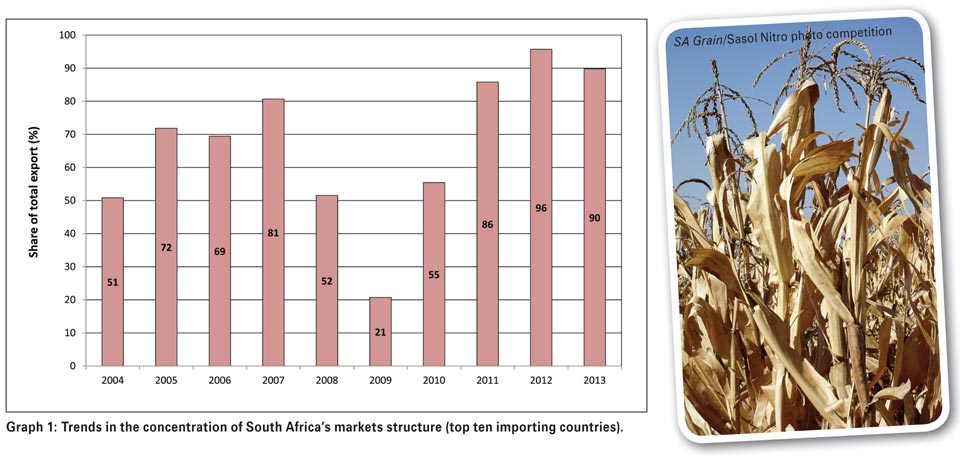

Maize market structure

Graph 1 shows that in the past three years, South African maize exports become more concentrated; meaning that a large quantity of South African maize have been increasingly going to a few countries. However, this was not the case ten years ago; evidently in 2004 the top ten South African importing countries accounted for approximately 51% of the total exports (ITC, 2014).

This means that South African maize export markets were wide, hence a positive view for market development and/or expansion. Over the years this trend continued at a volatile pace; with 2007 data showing that the top ten South African importing countries accounted for approximately 81% of the total exported quantity, and so becoming more concentrated (ITC, 2014).

In 2009, South African maize exports were wide, only 21% of the total maize went to the top ten importing countries. However, the past three years’ data shows that maize export markets became highly concentrated; with the 2011, 2012 and 2013 top ten importing countries accounting for 86%, 96% and 90%, respectively (Graph 1). This trend basically shows that a greater percentage of South African exports went to few countries (markets became concentration).

High market concentration tends to increase the level of dependency to few importers. Evidently, the current crop (2014/2015 maize) is showing a slow export pace, owing to slow demand from the few traditional importing nations coupled with the slow harvest rate, consequently driving down the prices.

Recently, South Africa largely exported to Mexico, Japan, Taiwan, Zimbabwe and BLNS (Botswana, Lesotho, Namibia and Swaziland). For the current season, Mexico is said to be having a good domestic crop and Zimbabwe is likely to import from Zambia (Zambia is said to be having a good crop), hence the soft demand.

East African export opportunities

Among many East African maize consuming countries, Kenya is noted to be the current leading importer, thus the focus of this article.

Recent reports from the International Grain Council have repeatedly reported about the expected maize demand in Kenya. This expected demand is mainly due to Kenyan declining domestic production, owing to erratic rains (BMI, 2014).

Kenya’s total cereal production decreased by 17% year-on-year for 2013/2014, meaning the production came down from 3,6 million tons to 2,8 million tons. The same year, Kenyan domestic consumption was at 3,8 million tons, meaning the demand for imports were 200 000 tons.

Furthermore, in 2014/2015 Kenyan maize production is expected to remain at low levels of 2,9 million tons, with consumption expected to be at 3,8 million tons; consequently the expected demand for imports is 900 000 tons (BMI, 2014).

Moreover, Table 1 shows that from 2015 to 2018 Kenyan maize production is expected to slightly increase. At the same time, consumption is expected to also show a steady increasing trend, owing to an expected increase in demand from the livestock sector due to the demand for meat.

Conclusion

Why is high concentration a concern for South African maize exports? The country needs as many markets as possible to avoid the risk of depending on a few importing countries. South African maize export markets are concentrated; therefore there is a need to increase the export market share (look for new opportunities).

Given the expected import demand in Kenya, which makes the country a long term maize net importer, this makes it an ideal market for South African maize. However, there are still some barriers to access the Kenyan maize market which needs to be addressed at governmental level, namely GMO issues.

At the same token, Global Biotech Update (2014) recently (on 11 June 2014) reported that the Kenyan governors are calling for a lifting of the GMO ban in the country, consequently making Kenya a potential market for South African maize.

Publication: August 2014

Section: On farm level