- Follow us:

- Our Commodities:

-

February 2014

WANDILE SIHLOBO, FUNZANI SUNDANI AND PETRU FOURIE, ECONOMISTS: INDUSTRY SERVICES, GRAIN SA

Since 9 December 2013, there have been significant increases in the domestic grain market. The main factors behind these movements have been the exchange rate, old season stock levels in the USA, weather conditions in South America as well as the demand from Asia and Africa.

International markets

Maize

On the international markets, much focus has been on the recent US maize ending stocks for 2013/2014 that are projected at 406 400 000 tons, which is 40 894 tons lower than the previous estimate (WASDE, 2014). There have been some major concerns about the rejection of US maize by China, due to unapproved GMO variety (International Grains Council [IGC], 2014).

In 2013, China rejected about 601 000 tons of US maize and maize by-products. In South America, plantings in Argentina made limited progress, with seeding finished on 4,4 million hectares (IGC, 2014).

Earlier rains in Argentina did help on the drought-affected crops; however the return of dry, hot weather has raised some major concerns about the yield prospects. In Brazil, after harsh, dry conditions in the early stages of planting; recent rains were favourable for full season 2013/2014 maize production.

Soybean

According to World Agricultural Supply and Demand Estimates (WASDE) (2014) global soybean production for 2013/2014 is estimated at a record of 286,8 million tons, up by 1,9 million tons; with major gains coming from the US and Brazil. US 2013/2014 soybean production is estimated to reach a record of 88,7 million tons (WASDE, 2014). At the same time, Brazilian soybean production is estimated to increase by 1 million tons to a record of 89 million tons; much of the increase is due to the increased area that was planted.

Brazil starts harvesting in March and Argentina in April and it is expected that price relief will be experienced from the end of February. In Argentina, 2013/2014 soybean production is estimated to be 57,5 million tons, which is higher than last year’s production of 49,3 million tons (IGC, 2014).

On the other hand, there has also been consisted export demand in the world market, with a large stake coming from China. China has recently purchased about 350 00 tons of US soybeans.

Wheat

Analysis shows that global 2013/2014 wheat supplies have increased by 1,5 million tons to 888,8 million tons. A large part of production is expected from China and Russia. For 2013/2014 wheat production, China is expected to increase by

1 million tons, at the same time in Russia, wheat production is expected to increase by 300 000 tons. In the US, cold weather temperatures have been a major concern for their winter wheat production (IGC, 2014).

In South America, production is expected to decrease with 500 000 tons in Argentina, due to an expected decrease in the harvested area. In the European Union, 2013/2014 wheat production is expected to decrease by 200 000 tons, with slight downward revisions for the United Kingdom, Finland and Denmark (WASDE, 2014).

Increasing demand is still observed from Egypt, Algeria, Japan and Syria (IGC, 2014). The IGC (2014) further noted that favourable weather conditions in India contributed to a 6% year-on-year increase in the area planted, thus an expected increase in production. Some traders are of the view that the government’s production target of 92,5 million tons in India is going to be exceeded.

Macroeconomic factors

Exchange rate

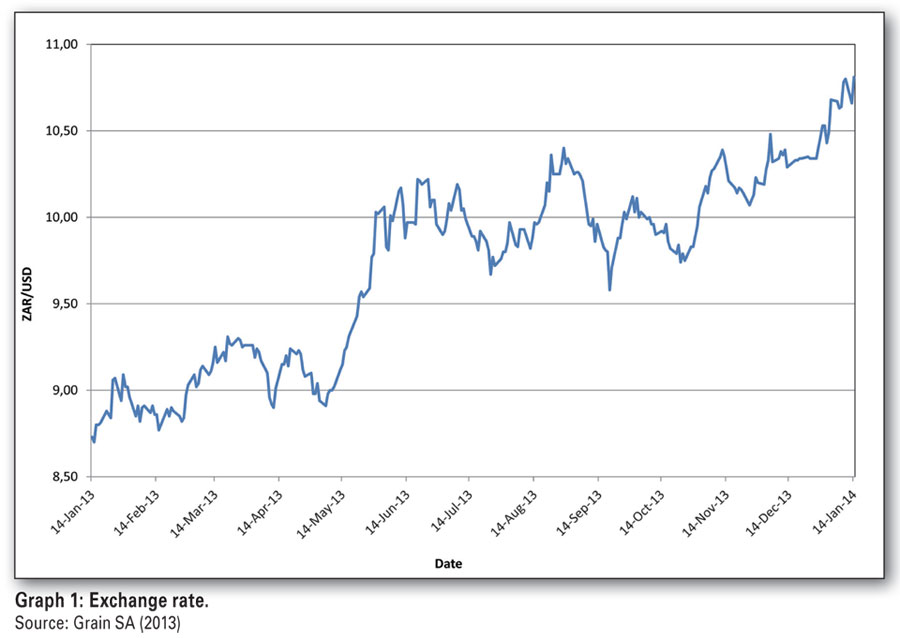

During the past month, the rand has significantly weakened against most major currencies, reaching the high levels of R10,81 to the US dollar on 14 January 2014. From 14 January 2013 to 14 January 2014, the South African rand has weakened by approximately 23%; from R8,73 to R10,81.

There are a number of domestic factors that have contributed to the significant weakening of the rand value, ranging from the widening current account and budget deficit to global economic conditions, but the most recent one was the announcement by the United States Federal Reserve bank (US Fed) of the start of bond tapering this month (Nedbank Group Economic Unit, 2014).

The US Fed decided to reduce the size of its asset purchasing programme of billion by billion to billion with effect from January 2014.

Currently, the US economy have been gaining strong momentum; with recent manufacturing data coming out stronger than expected, hence paving up a way for the US Fed to start with the stimulus tapering (Nedbank Group Economic Unit, 2014). There are still some expectations that the rand will continue to trade at low levels, due to concerns about further labour unrests, widening current account and budget deficit as well as the uncertainty of the outcome of the upcoming elections.

On the other hand, the weak rand supports domestic commodity prices (yellow maize, white maize, soybean etc), thus sparking up gains from the exporting commodities.

Domestic factors

Growing conditions in maize producing areas

The eastern part of the country (Mpumalanga and Eastern Free State) where yellow maize is predominantly planted looks good in general, with follow-up rains frequently occurring. In small areas of Mpumalanga too much rain occurred, leading to some waterlogging; however the extent of the damage to the crops is not so detrimental.

The western parts of the country, more specifically the North West Province started off with a very dry season and almost no underground moisture. Thankfully rain occurred during the beginning of December making it possible for producers to plant, although the subsurface moisture has still not recovered. Seedlings are currently very small. Some areas in the North West Province are reported to be very dry, where follow-up rain remains very critical.

In general, conditions look favourable in the North Western Free State and Central Free State although the Hertzogville/Hoopstad area did not receive enough rain which led to producers planting less than they had anticipated. The western parts of the country require and are dependent on follow-up rain.

Wheat

Producers in the Western Cape completed their wheat harvest during the end of last year. Producers in the Swartland region achieved good yields although some grading problems were experienced. In Caledon, Krige, Rietpoel and Klipdale the rain during harvest time caused grading problems mainly due to the falling number and sprouting.

The wheat however did surprisingly well as compared to what was expected. Producers in Bredasdorp and Mossel Bay finished harvesting before any rainfall occurred; good wheat yields and grades were achieved. In the Eastern Free State, rains were good for the summer crops although it had a negative impact on the winter crops which led to producers harvesting low quality wheat.

Parity prices

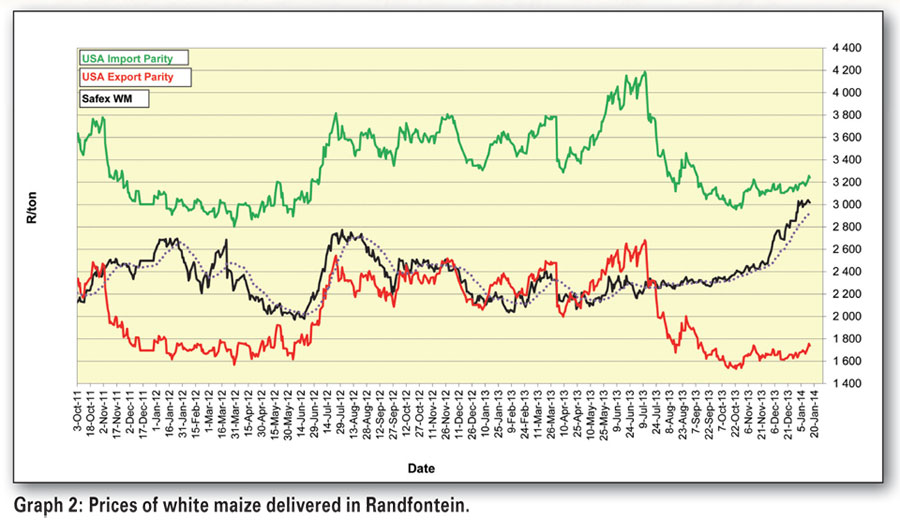

Graph 2 show prices for old season white maize, Safex maize prices showed a huge increase during the December holidays for the old season crop. Much of this increase was due to the increasing demand from the African countries, weakening of the exchange rate as well as tight old stocks. White maize prices are currently trading at R3 018/ton which is 12% higher compared to price levels seen 17 December last year.

South Africa has already exported about 145 996 tons of white maize to Zimbabwe. Indicators show that production conditions in Zimbabwe are poor and that more imports are needed. Zambia does not have sufficient maize for exports to Zimbabwe.

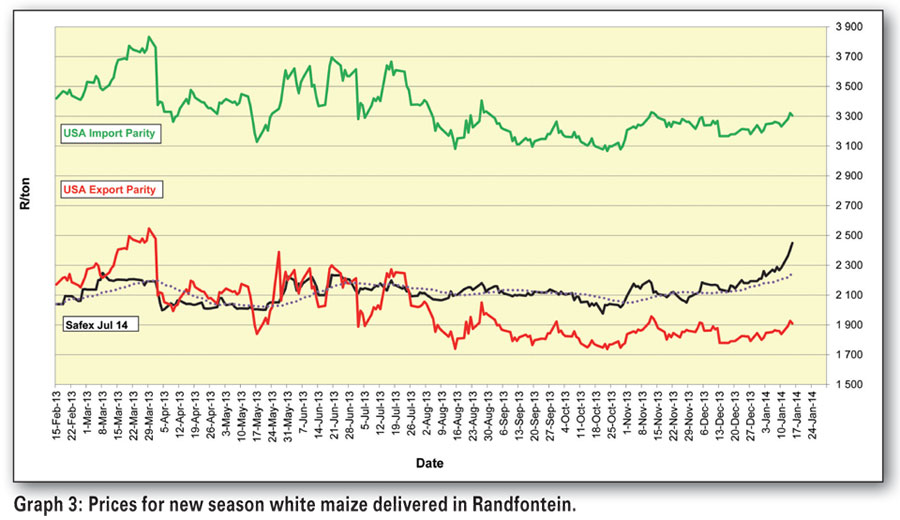

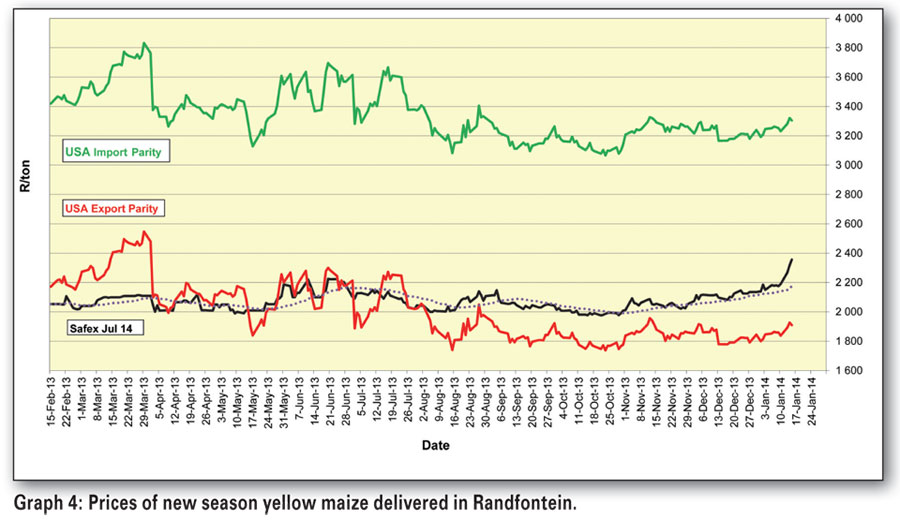

Graph 3 and Graph 4 show prices of new season white and yellow maize. White maize prices for delivery in July are currently trading at R2 449/ton which is 18% higher compared to price levels seen 17 December last year. Yellow maize prices for delivery in July are currently trading at R2 356/ton which is 13% higher compared to price levels seen

17 December last year.

New season prices are supported by prospects of tight stocks as well as uncertain weather conditions in the western producing areas.

Producers should take note that the weak rand value supports the domestic price levels of maize. Furthermore, beware that South America starts harvesting soybean in March, which may put international commodity prices under pressure.

The USA HRW prices are currently at normal price levels, which may lead to the triggering of the South African wheat tariff if prices decline further.

Further reading

United States Department of Agriculture, 2014. World agricultural supply and demand estimate. USDA. Washington.

International Grain Council, 2014. Grain market indicators. IGC. London.

Grain SA, 2014. Industry service: Market reports. Grain SA. Pretoria.

Publication: February 2014

Section: Markoorsig