- Follow us:

- Our Commodities:

-

December 2014

|

|

||

|

The reporting period was distinguished by important objectives reached, support to grateful stakeholders in the value chain and characterised by new challenges introduced by the policy, regulatory and industry environment. Market information Access to the public Access to timely information for all the stakeholders involved in the supply chain is a prerequisite for the efficient functioning of the free market. Through prices, the consumer signals to the producer how much to plant. Through price signals demand rationing took place when the rate of commodity exports increased above available supply. Prices signal to consumers when break even cost levels are reached that may lead to a decline in future production. Access to reliable and accurate information is thus especially important to the consumer and with respect to food security. The value of Grain SA’s market information to the public is acknowledged by the following comments received from value chain partners on the accessibility, objectiveness and accuracy of the information:

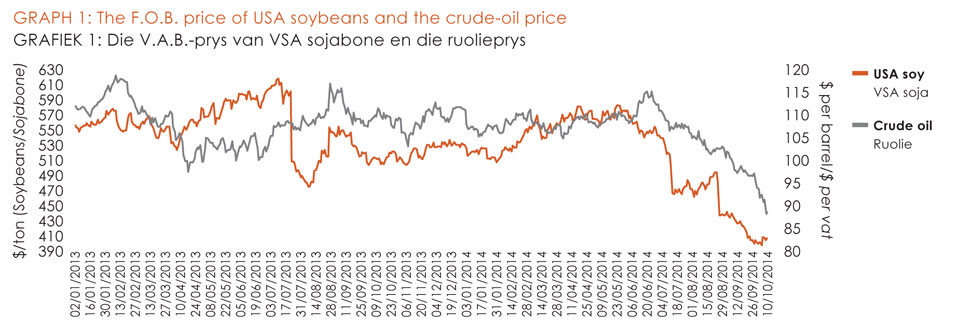

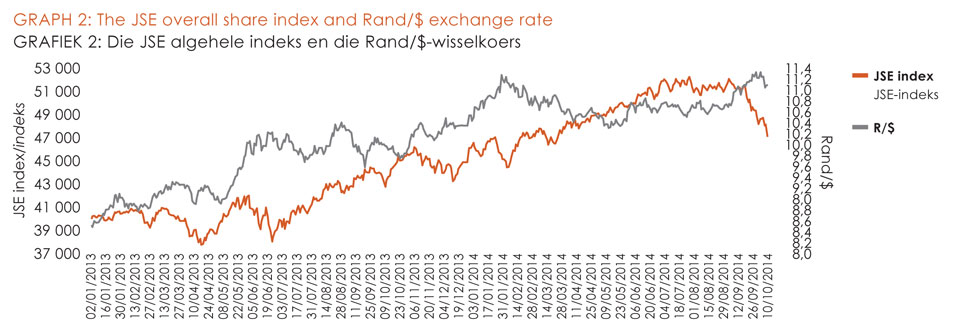

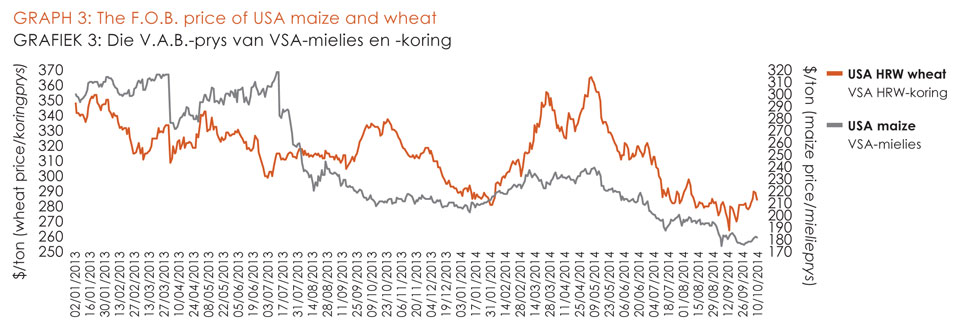

The accessibility of this information assists our government institutions and universities to evaluate the reasons for the increase of maize prices from export parity price levels to import parity price levels during the past year. The unforeseen export of maize to Zimbabwe and the resultant impact on food prices was explained, as well as the price decline following the early deliveries of maize. Daily data capturing, analysis and information The information on grain and oilseeds was improved by introducing a model to derive the crush margin for soybeans providing more clarity on this developing market. Additional price data on commodities trading in China and Japan were introduced as the USA is not the only important region determining world prices for commodity exports. We also improved our focus on analysing the domestic market, thereby enabling us to be less reliable on external opinions and reports. Supplying objective, accurate and reliable information to public and private stakeholders ensured excellent collaboration amongst industry role-players on the sharing of information. Our reports are tweeted to followers on social media providers, such as Twitter@GrainSA and posted on our website daily. We also send the information by email to each of our members daily. Market overview The JSE Overall Share Index (Graph 2) was in October 2014, 9% higher than a year ago, while the gold price and Brent crude oil prices (Graph 1) decreased by 4% and 20% respectively. In January 2014, the USA Federal Reserve started reducing its quantitative easing contributions to the USA economy and that led to a strong dollar compared to the euro. The dollar further gained support due to expected interest rate hikes in early 2015. However a strong dollar depends on an improvement in the USA economy. The strengthening of the dollar and increases in world supplies had a negative impact on agricultural commodity prices. Since October 2013, CBOT maize and soybean prices decreased by 15%, and wheat 21%, respectively. The outlook for global commodity prices is still bearish, as South America and the Black Sea countries also have large supplies. Unfavourable weather conditions during harvesting in the USA provided some support in the short term during October 2013. The weak rand supported domestic agricultural commodity prices, but new season crop prices were negatively influenced by large carry-out. Since October 2013, the rand depreciated 11% against the dollar (Graph 2). The rand depreciated due to the negative balance of payments, labour unrest, low economic growth, domestic policy uncertainty and global policy environment. |

Die verslagtydperk is gekenmerk deur belangrike doelwitte wat bereik is, steun aan dankbare belanghebbendes in die waardeketting, en nuwe uitdagings wat deur die beleids-, regulatoriese en bedryfsomgewing gestel is. Markinligting Toegang tot die publiek Toegang tot tydige inligting vir al die belanghebbendes betrokke by die voorsieningsketting is ‘n voorvereiste vir die doeltreffende funksionering van die vrye mark. Deur pryse lig die verbruiker die produsent in oor hoeveel om te plant. Deur prysseine het vraagrantsoenering plaasgevind toe die koers van kommoditeitsuitvoere hoër as die beskikbare aanbod gestyg het. Pryse dui vir verbruikers aan wanneer gelykbreekkostevlakke bereik word wat tot ‘n daling in toekomstige produksie kan lei. Toegang tot betroubare en akkurate inligting is dus veral belangrik vir die verbruiker en ten opsigte van voedselsekerheid. Die waarde van Graan SA se markinligting aan die publiek word erken in die volgende kommentaar oor die toeganklikheid, objektiwiteit en akkuraatheid van die inligting wat van waardekettingvennote ontvang is:

Die toeganklikheid van hierdie inligting help ons staatsinstellings en universiteite om die redes vir die styging in mieliepryse oor die afgelope jaar van uitvoerpariteitsprysvlakke tot invoerpariteitsprysvlakke te evalueer. Die onvoorsiene uitvoer van mielies na Zimbabwe en die gevolglike impak op voedselpryse is verklaar asook die prysdaling ná die vroeë lewering van mielies. Daaglikse datavaslegging, ontleding en inligting Die inligting oor graan en oliesade is verbeter deur ‘n model bekend te stel om die persmarge vir sojabone af te lei, wat meer duidelikheid oor hierdie ontwikkelende mark verskaf het. Bykomende prysdata oor kommoditeitsverhandeling in China en Japan is bekend gestel, aangesien die VSA nie die enigste belangrike streek is wat wêreldpryse vir kommoditeitsuitvoere bepaal nie. Ons het ook ons fokus op die ontleding van die plaaslike mark verbeter, wat ons in staat stel om minder op eksterne menings en verslae staat te maak. Die verskaffing van objektiewe, akkurate en betroubare inligting aan openbare en privaat belanghebbendes het uitstekende samewerking onder bedryfsrolspelers oor die deel van inligting verseker. Ons verslae word aan volgelinge getwiet op sosialemedia-verskaffers soos Twitter@GrainSA, en daagliks op ons webtuiste geplaas. Ons stuur ook daagliks inligting per e-pos aan elkeen van ons lede. Markoorsig Die JSE Oorkoepelende Aandele-indeks (Grafiek 2) was 9% hoër in Oktober 2014 as ‘n jaar gelede, terwyl die goudprys en die prys van Brent-ruolie (Grafiek 1) onderskeidelik met 4% en 20% gedaal het. In Januarie 2014 het die VSA se Federale Reserwebank begin om sy kwantitatiewe verligtingsbydraes tot die Amerikaanse ekonomie te verminder, en dit het tot ‘n sterk dollar gelei, vergeleke met die euro. Die dollar het verder steun gekry as gevolg van verwagte rentekoersverhogings vroeg in 2015. ‘n Sterk dollar hang egter van ‘n verbetering in die VSA-ekonomie af. Die versterking van die dollar en toename in wêreldvoorrade het ‘n negatiewe uitwerking op landboukommoditeitspryse gehad. Sedert Oktober 2013 het CBOT-mielie- en sojaboonpryse met 15% en koringpryse met 21% gedaal. Die vooruitsigte vir wêreldwye kommoditeitspryse is steeds aan die daal, aangesien Suid-Amerika en die Swartsee-lande ook groot voorrade het. Ongunstige weerstoestande in die oestyd in die VSA het in Oktober 2013 ‘n mate van steun in die kort termyn gebied. Die swak rand het plaaslike landboukommoditeitspryse ondersteun, maar die nuwe seisoen se gewaspryse is negatief deur groot oordragvoorrade geraak. Sedert Oktober 2013 het die rand met 11% teen die dollar verswak (Grafiek 2).Die rand het verswak as gevolg van die negatiewe betalingsbalans, arbeidsonrus, lae ekonomiese groei, onsekerheid oor binnelandse beleid, en die wêreldwye beleidsomgewing. |

|

|

|

||

|

|

||

|

Summer grain A recovery in sorghum production led JSE prices for sorghum to trade at R2 480 per ton in October, which is 28% lower compared to a year ago. Sorghum prices were affected negatively by record maize yields. Due to sufficient production no imports, as compared to the previous year when 50 000 tons of sorghum had to be imported, are foreseen. The International Grains Council (IGC) forecasted the 2014/2015 world sorghum production at 63,3 million tons. This is deemed to be the highest production since 2008/2009, owing to increases in Australia, USA and Argentina. White maize prices traded at R1 874 per ton, which is 20% lower than a year ago. Yellow maize prices traded at R1 885 per ton, which is 12% lower than a year ago. During October 2014 the new crop futures prices for delivery in July 2015 were respectively 7% lower for white maize and 4% lower for yellow maize compared to a year ago. In October 2014, the total South African carry-out for white and yellow maize for the 2014/2015 marketing year was aimed at 2 117 000 tons compared to 589 000 tons in the previous marketing year. The projected total surplus above the pipeline reached 916 000 tons, compared to a shortage of 573 000 tons above the pipeline the previous year. The recovery in South African production, coupled with insufficient export demand for white maize resulted in lower white maize prices. Yellow maize exports corresponded with that of the previous marketing year. New crop yellow maize prices experienced price pressure due to a recovery in USA new season crop supplies (Graph 3) and a recovery in South African maize production. |

Somergraan ‘n Herstel in sorghumproduksie het daartoe gelei dat JSE-pryse vir sorghum in Oktober teen R2 480 per ton verhandel het, wat 28% laer was as ‘n jaar vantevore. Sorghumpryse is negatief geraak deur rekordmielieopbrengste. As gevolg van voldoende produksie word geen invoere in die vooruitsig gestel nie, vergeleke met die vorige jaar se 50 000 ton sorghum wat ingevoer moes word. Die Internasionale Graanraad (IGC) het voorspel dat 2014/2015 se wêreldwye sorghumproduksie 63,3 miljoen ton sal wees. Dit word as die hoogste produksie sedert 2008/2009 beskou as gevolg van stygings in Australië, die VSA en Argentinië. Witmielies het teen R1 874 per ton verhandel, wat 20% laer is as ‘n jaar gelede. Geelmielies het teen R1 885 per ton verhandel, wat 12% laer is as ‘n jaar gelede. In Oktober 2014 was die nuwe gewastermynkontrakpryse vir lewering in Julie 2015, 7% laer vir witmielies en 4% laer vir geelmielies as ‘n jaar gelede. In Oktober 2014 was die totale Suid-Afrikaanse oordragvoorradesyfer vir wit- en geelmielies vir die 2014/2015-bemarkingsjaar op 2 117 000 ton gemik, vergeleke met 589 000 in die vorige bemarkingsjaar. Die geprojekteerde totale surplus bo die pyplyn het 916 000 ton bereik, vergeleke met ‘n tekort van 573 000 bo die pyplyn die vorige jaar. Die herstel in Suid-Afrikaanse produksie, tesame met ‘n onvoldoende uitvoervraag na witmielies, het tot laer witmieliepryse gelei. Geelmielie-uitvoere het met dié van die vorige bemarkingsjaar ooreengestem. Die nuwe oes geelmielies se pryse het prysdruk ervaar as gevolg van ‘n herstel in die VSA se gewasvoorrade vir die nuwe seisoen (Grafiek 3) en die herstel van Suid-Afrika se mielieproduksie. |

|

|

|

||

|

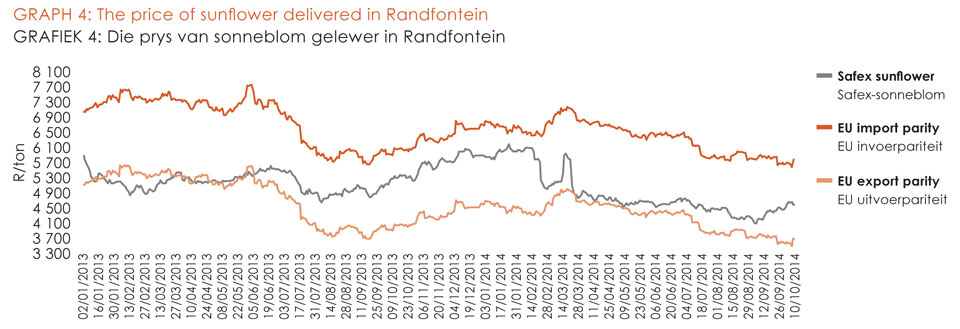

Oilseeds The domestic prices for oilseeds were largely supported by an increased demand from the newly introduced crushing capacity. Our estimates showed that South Africa’s soybean imports may exceed 100 659 tons due to an increased demand and insufficient soybean production. In October 2014 soybean prices traded at R5 110 per ton, which is 10% lower than a year ago. Domestic production increased from 784 500 tons in the 2013/2014 marketing year to 944 340 tons in the 2014/2015 marketing year. South African soybean imports may stabilise at 100 700 tons in 2014/2015, given that the projected soybean to be crushed for oil and oilcake remain at 720 000 tons, and full fat soybean consumption at 130 000 tons. Sunflower seeds traded around R4 585 per ton in October 2014, which is 14% lower than a year ago (Graph 4). Domestic production increased from 557 000 tons in 2013/2014 to 853 325 tons in 2014/2015. |

Oliesade Die plaaslike pryse vir oliesade is grootliks deur ‘n groter vraag na die pas-ingestelde perskapasiteit ondersteun. Ons skattings toon dat Suid-Afrika se sojabooninvoere 100 659 ton kan oorskry as gevolg van ‘n groter vraag en onvoldoende sojaboonproduksie. In Oktober 2014 het sojabone teen R5 110 per ton verhandel, wat 10% laer is as ‘n jaar gelede. Plaaslike produksie het van 784 500 ton in die 2013/2014-bemarkingsjaar tot 944 340 ton in die 2014/2015-bemarkingsjaar toegeneem. Suid-Afrika se sojabooninvoere kan in 2014/2015 op 100 700 ton stabiliseer, gegewe dat die geprojekteerde hoeveelheid sojabone wat vir olie en oliekoek gebreek word op 720 000 ton, en volvet-sojaboonverbruik op 130 000 ton bly. Sonneblomsaad het in Oktober 2014 teen ongeveer R4 585 per ton verhandel, wat 14% laer is as ‘n jaar gelede (Grafiek 4). Plaaslike produksie het van 557 000 ton in 2013/2014 tot 853 325 ton in 2014/2015 toegeneem. |

|

|

|

||

|

The carry-out for sunflower seeds may reach 118 300 tons at the end of 2014/2015 and prices may enjoy underlying support at a deficit above the pipeline of 84 000 tons. The domestic sunflower production increased and it is expected that the projected consumption will also increase. The oilseeds industry imported approximately 123 503 tons of sunflower oil in 2013. Since October a year ago, the international price of sunflower seed from the European Union (EU) countries decreased by 17%. South African sunflower seed prices decreased by 14%. Global sunflower seed prices may recover due to an expected decline in sunflower seed production in the Black Sea region. The carry-out for groundnuts increased to 15 100 tons due to increased production. The 2014/2015 production is estimated at 78 090 tons, with an average national yield of 1,5 tons per hectare. Consequently groundnut imports may decrease to 8 000 tons, while exports may increase to 20 000 tons compared to 10 400 tons the previous marketing year. The commercial delivery of canola is expected to increase by 31% in 2014/2015, compared to the previous marketing year. The commercial supply of canola increased due to a 32% increase in plantings and an opening stock level of 26 900 tons. The carry-out for 2014/2015 may increase to 66 000 tons if commercial demand remains around the level of 108 000 tons. Winter grain Wheat traded at R3 598 per ton during the second week of October 2014, which is only 4% higher than a year ago. Despite ample global supplies, wheat prices managed to gain some momentum, owing to an increase in demand, quality concerns in the EU, as well as unfavourable weather conditions in Australia and Canada. To meet local wheat demand of 3 150 000 tons South Africa may need to import almost 1,7 million tons of wheat in the 2014/2015 marketing year. South Africa is a net wheat importing country. The price of malting barley is determined by a single barley buyer and is linked to the Safex wheat price in order to enable transparent price discovery, as well as the hedging of prices. The demand for malting barley aims at 345 000 tons. Due to an expected recovery in production, South Africa may import less malting barley in 2014/2015. Export promotion Development of new markets Grain SA identified the Middle East as a region, which poses excellent opportunities to establish a permanent market for commodity exports. The region includes countries, such as Saudi Arabia and Iran that respectively import about 1,8 million tons and 8 million tons annually. The Iranian authorities would like to see the sanctions by the EU, USA and the United Nation Security Council lifted considering the tremendous impact they had on the Iranian economy. Grain SA visited Tehran at the end of November 2014 and discussed the possibilities of commodity exports with the Iranian Chamber of Commerce, Industries and Mines (ICCM), the Government Trading Corporation of Iran (GTC), State Livestock Affairs Logistics Ministry of Jahad Agriculture (SLAL) and Golbahar Daneh. Grain SA also visited Aldahra in the United Arab Emirates. Except for Israel and Iran, the company trades with all the countries in the Middle East. In collaboration with the Department of Agriculture, Forestry and Fisheries (DAFF) and SACOTA, the export of a consignment of maize of 51 000 tons to Saudi Arabia were enabled. Prospectus on the South African Maize Industry In furthering exports, Grain SA collaborates with value chain partners, including the ARC, AFMA, GSI, JSE, NCM, SACOTA, SANSOR, SAPA, SAGL and Tongaat Hulett Starch in finalising the Prospectus on the South African Maize Industry. The prospectus covers the broader descriptive issues of maize and its uses in South Africa, the procedural issues of the marketing of maize and the more specific issues of grain quality, grain standards, exporting facilities, logistics, required export documentation and the management of price risk in South Africa. The objective of the prospectus is to promote South African maize for export purposes abroad. Import replacement and industry development Finalising the biofuel regulations for sorghum, canola, soybean and sunflower The Department of Energy (DOE) introduced a biofuels implementation committee to oversee the finalisation and implementation of the biofuel regulations. On the request of Grain SA a sub-committee on feedstock issues were established. Grain SA chairs this committee, representing all possible feed stocks for biofuel purposes, including grain sorghum, canola, soybeans, sugar and other lesser-known feed stocks. We submitted important inputs in support to the DAFF and the DOE to ensure future feasible regulations that support the production of feedstock. The biofuel regulations need to be finally discussed with stakeholders, submitted to cabinet and then published in the Government Gazette for implementation. Crushing plants: Oilseeds According to the Protein Research Foundation (PRF) the total soybean crushing capacity in South Africa measured in 2012 only 600 000 tons as represented by five crushing plants at the time. By 2013/2014 the new crushing capacity introduced by five different companies measured just more than 1,5 million tons. The total crushing capacity aims at 2 102 000 tons in 2014. The total full fat production capacity aims at 580 000 tons. The PRF states that the current soybean meal demand is 1,3 million tons, which is equal to 1,63 million tons of soybeans. The 2015 soybean meal demand may increase to 1,6 million tons and is equal to a demand of nearly 2 million tons of soybeans. By 2020 the soybean meal demand may exceed 1,82 million tons or may equal a demand of 2,3 million tons of soybeans. The newly introduced crushing capacity is expected to substitute the growing imports of oilcake and vegetable oil and to increase the production of soybeans, sunflower seed and canola. To date the following increased crushing of oilseeds has been witnessed (Table 1): |

Die oordragvoorradesyfer vir sonneblomsaad kan aan die einde van 2014/2015 118 300 ton bereik, en pryse kan onderliggende steun geniet teen ‘n tekort van 84 000 ton bo die pyplyn. Plaaslike sonneblomproduksie het toegeneem en na verwagting sal die geprojekteerde verbruik ook toeneem. Die oliesadebedryf het in 2013 ongeveer 123 503 sonneblomolie ingevoer. Sedert Oktober ‘n jaar gelede het die internasionale prys van sonneblomsaad uit die Europese Unie (EU) met 17% gedaal. Suid-Afrikaanse sonneblompryse het met 14% gedaal. Wêreldwye sonneblompryse kan herstel as gevolg van ‘n verwagte daling in sonneblomproduksie in die Swartsee-streek. Die oordragvoorradesyfer vir grondbone het as gevolg van verhoogde produksie tot 15 100 ton gestyg. Die 2014/2015-produksie word op 78 090 ton geskat, met ‘n gemiddelde nasionale opbrengs van 1,5 ton per ha. Grondbooninvoere kan gevolglik tot 8 000 ton daal, terwyl uitvoere tot 20 000 ton kan toeneem, vergeleke met 10 400 ton in die vorige bemarkingsjaar. Die kommersiële lewering van kanola sal na verwagting in 2014/2015 met 31% styg, vergeleke met die vorige bemarkingsjaar. Die kommersiële aanbod van kanola het gestyg as gevolg van ‘n 32% toename in aanplantings en ‘n aanvangsvoorraadvlak van 26 900 ton. Die oordragvoorradesyfer vir 2014/2015 kan tot 66 000 ton toeneem indien kommersiële vraag min of meer op die vlak van 108 000 ton bly. Wintergraan Koring het in die tweede week van Oktober 2014 teen R3 598 per ton verhandel, wat slegs 4% hoër as ‘n jaar gelede is. Ondanks voldoende wêreldwye voorrade het koringpryse dit reggekry om as gevolg van ‘n toename in vraag, kommer oor gehalte in die EU, en ook ongunstige weerstoestande in Australië en Kanada momentum te kry. Om in die plaaslike koringvraag van 3 150 000 ton te voorsien, moet Suid-Afrika dalk bykans 1,7 miljoen ton koring in die 2014/2015-bemarkingsjaar invoer. Suid-Afrika is ‘n netto koringinvoerland. Die prys van moutgars word deur ‘n enkele garskoper bepaal, en dit word aan die Safex-koringprys gekoppel ten einde deursigtige prysbepaling en die verskansing van pryse moontlik te maak. Die vraag na moutgars mik na 345 000 ton. As gevolg van ‘n onverwagte herstel in produksie kan Suid-Afrika dalk in 2014/2015 minder moutgars invoer. Uitvoerbevordering Ontwikkeling van nuwe markte Graan SA het die Midde-Ooste geïdentifiseer as ‘n streek wat uitstekende geleenthede bied om ‘n permanente mark vir kommoditeitsuitvoere te vestig. Die streek sluit lande soos Saoedi-Arabië en Iran in, wat onderskeidelik ongeveer 1,8 miljoen en 8 miljoen ton jaarliks invoer. Die Iranse owerhede wil graag hê dat die sanksies deur die EU, VSA en die VN Veiligheidsraad opgehef moet word in die lig van die geweldige impak wat dit op die Iranse ekonomie het. Graan SA het Teheran aan die einde van November 2014 besoek en die moontlikhede van kommoditeitsuitvoere met die Iranse Kamer van Koophandel, Nywerhede en Myne (ICCM), die staatshandelskorporasie van Iran (GTC), die Staatslewendehawe Sakelogistiek-ministerie van Jahad-landbou (SLAL) en Golbahar Daneh bespreek. Graan SA het ook Aldahra in die Verenigde Arabiese Emirate besoek. Buiten Israel en Iran, dryf die maatskappy handel met al die lande in die Midde-Ooste. In samewerking met die Departement van Landbou, Bosbou en Visserye (DLBV) en SACOTA is die uitvoer van ‘n besending van 51 000 ton mielies na Saoedi-Arabië moontlik gemaak. Prospektus oor die Suid-Afrikaanse Mieliebedryf Ten einde uitvoere te bevorder, werk Graan SA met waardekettingvennote soos die LNR, AFMA, GSI, JSE, NCM, SACOTA, SANSOR, SAPV, SAGL en Tongaat Hulett Starch saam om die Prospektus oor die Suid-Afrikaanse Mieliebedryf te finaliseer. Die prospektus dek die wyer beskrywende kwessies oor mielies en die gebruik daarvan in Suid-Afrika, die prosedurele kwessies ten opsigte van die bemarking van mielies en die meer spesifieke kwessies van graangehalte, graanstandaarde, uitvoergeriewe, logistiek, vereiste uitvoerdokumentasie en die bestuur van prysrisiko in Suid-Afrika. Die doel van die prospektus is om Suid-Afrikaanse mielies vir uitvoerdoeleindes oorsee te bevorder. Invoervervanging en bedryfsontwikkeling Finalisering van die biobrandstofregulasies vir sorghum, kanola, sojaboon en sonneblom Die Departement van Energie (DVE) het ‘n biobrandstofimplementeringskomitee aangestel om oor die finalisering en implementering van die biobrandstofregulasies toesig te hou. Op versoek van Graan SA is ‘n subkomitee vir grondstofkwessies aangestel. Graan SA is voorsitter van hierdie komitee, wat alle moontlike grondstowwe vir biobrandstofdoeleindes verteenwoordig, insluitende graansorghum, kanola, suiker en ander minder bekende grondstowwe. Ons het belangrike insette ter ondersteuning by die DLBV en DVE ingedien om haalbare regulasies vir die toekoms te verseker wat die produksie van grondstowwe ondersteun. Die biobrandstofregulasies moet finaal met belanghebbendes bespreek word, aan die kabinet voorgelê en dan in die Staatskoerant gepubliseer word sodat dit geïmplementeer kan word. Persaanlegte: Oliesade Volgens die Proteïennavorsingstigting (PNS) was die totale sojaboonperskapasiteit in Suid-Afrika in 2012 slegs 600 000 ton, verteenwoordig deur vyf brekingsaanlegte op daardie tydstip. Teen 2013/2014 was die nuwe perskapasiteit met vyf nuwe maatskappye net meer as 1,5 miljoen ton. Die totale perskapasiteit se doelwit is 2 102 000 ton in 2014. Die totale volvet-produksiekapasiteit se doelwit is 580 000 ton. Die PNS het aangekondig dat die huidige sojameelvraag 1,3 miljoen ton is, wat gelyk is aan 1,63 miljoen ton sojabone. Die 2015-vraag na sojameel kan tot 1,6 miljoen ton toeneem en is gelyk aan ‘n vraag van bykans 2 miljoen ton sojabone. Die 2020-vraag na sojameel kan meer as 1,82 miljoen ton wees en gelyk wees aan ‘n vraag van bykans 2,3 miljoen ton sojabone. Die pas ingestelde perskapasiteit sal na verwagting die groeiende invoer van oliekoek en plantolie vervang en die produksie van sojabone, sonneblom en kanola verhoog. Tot op hede is die volgende verhoogde breking van oliesade aangeteken (Tabel 1): |

|

|

|

||

|

In order to gain market access the newly introduced plants market the domestically produced oilcake at a discount. Given the declining crush margin it is expected that the discount will cease to exist as soon as the teething problems in the newly created soybean crushing capacity are solved sufficiently. Trade and trade policy environment Wheat import tariff International Trade Administration Commission (ITAC) approved the application by Grain SA for a new reference price level of 4 per ton on 23 April 2013 instead of the previous 5 per ton. A wheat tariff was triggered when the FOB Gulf HRW No.2 wheat price decreased to a level of less than 4 per ton for three consecutive weeks in September. Although the tariff of R156 per ton is not sufficient to increase the producer price for wheat, it enables a more stable environment and certainty for producers to consider increased wheat production. Location differentials Numerous inputs were made since 2008 and before to address the functioning of the futures market and the location differential. Grain SA dedicated a significant amount of resources in focusing on the abolishment of the location differential during 2013 and 2014. When members were confronted with the probability that the organisation may succeed in the successful abolishment of the differential for a trial period of two years some reconsidered the impact of having no differentials. Consequently, Grain SA received counter proposals from other members to keep the differentials intact. The JSE took a business decision to keep the differential system, arguing that the differential system supports their business model and that the decision was taken in this respect. Grain SA does not support the JSE location differential system and is of opinion that it should be abolished. Although we do not support the differential, every effort is taken to keep it as low as possible. Therefore we will continue to monitor the fair calculation of the differential by the JSE and to continually engage with the JSE on the matter. The maize differential increased on average by 9,8% during March 2014. This followed after intense negotiations with the JSE and an original proposed increase of 12,9%. Grain SA saved producers more than R100 million. Furthermore, Grain SA indicated to the JSE that the maize location differential at Wesselsbron was published incorrectly. The JSE corrected the averaged rail versus road out-loading ratios. Including the updated ratios in calculations for the Wesselsbron differential, the latter is recalculated to be R15 per ton lower than the previously published rate. This relates to a potential saving to producers delivering maize at the Wesselsbron silo of about R4,125 million. Cash market transparency and basis trading Prof Mathew Roberts was commissioned by the National Agricultural Marketing Council (NAMC) in 2008 to investigate the functioning of the futures market. He indicated that the differential issue is a symptom of another problem, which is to address the transparency of cash market prices. Transparency with regard to cash market prices is lacking to a significant extent. The development of the cash market and transparency should be the focus in our future objectives to lessen the importance of the location differential in cash market transactions. Mr Arlan Suderman states that the transparent cash market is the best indicator of supply and demand fundamentals in the USA. Transparency is a necessary component for an accurate cash market that reflects true supply and demand fundamentals. Without that transparency, producers do not know if the price being offered will truly do the job of stimulating production, slowing demand or whatever is needed at the time. Without transparency, how can the end user know what price he needs to offer to encourage sufficient production or in some cases discourage production because supplies can be a liability. As such, transparency is a core value that is hold dear to role-players in the USA. Both the producers and end-consumers are continuously at loggerheads to make sure that a high level of transparency at all levels of the commodity markets is maintained. They are constantly working on new systems to report supply and demand data, while also reporting cash prices being offered and paid at all levels of the marketing system. Maize marketing year The marketing information year on supply and demand reporting for all winter grain is from October to September each year. Similarly, the marketing year for summer grain, except for maize, is from March to February. Grain SA proposed to the industry to adapt the marketing year for maize from March to February as well. The estimated potential early delivery figures and the resulting estimated ending stocks do have the potential to significantly impact the volatility of market prices. The proposed change to the maize marketing year will add to relieve this problem and support food security. Estimated stock levels at marketing year end determine market prices during the year. The uncertain figure in the annual supply and demand estimates, which has a significant weight during the months of March and April are the unpredictable early delivery figure. To change the marketing years means that the early delivery issue can be omitted in total and thereby ensuring increased predictability and market transparency for those role-players, such as producers that do not have the ability to predict the early delivery figures accurately. The average contribution (over a period of ten years from 2005 to 2014) of the early delivery figure as a percentage of closing stock levels are 34% and for the utilisation figure 31%. The early delivery figure reached a high of 81% deliveries as a percentage of ending stocks in 2014 and a low of 3% in 2006. The uncertainty on early deliveries can be omitted in total by changing the marketing year for information reporting purposes from instead of May to April to March to February. Grain SA’s supply and demand information will reflect this marketing period. Commitment of traders report Van der Vyfer and Meyer (2014) reported in their report – titled Positioning reporting by category in agricultural derivatives markets: Should South Africa follow international best practices? – that on the surface it appears that South Africa is in line with international practices. Internationally there is a drive to increase regulations on commodity markets, but more so, to improve transparency. Many analyses refer to the role and importance of information. Categorising positions taken (hedging or speculating) on the JSE Commodity Derivatives Market (JSE CDM) is inevitable according to the finding of this research, initiated by Grain SA, especially if the CDM wishes to be in line with international practices. However, it should be emphasised that liquidity on the CDM does not allow for the same detailed reports and initially it will probably be aggregate at a high level, but it could be a start. Without this data (over time) and the subsequent analysis that will flow from this, local policy makers could potentially again avoid the next financial meltdown and thereby the threat to food security through high commodity prices, but also production through low prices when the correct price signals do not reach producers. International trade The long-running Economic Partnership Agreement (EPA) negotiations between a group of Southern African Development Community (SADC) countries (Angola, Botswana, Lesotho, Mozambique, Namibia, South Africa and Swaziland) and the EU were finally concluded on 15 July 2014. Grain SA achieved to negotiate a limited tariff rate quota of 300 000 tons on imported wheat. Preference will be applicable in South Africa between 1 November and 31 January and in Namibia between 1 December and 28 February. For South Africa and Namibia, wheat as part of this quota can only be cleared through Durban, Richards Bay and Walvis Bay in future. Grading regulations Grading of soybeans The rapid expansion in soybean production puts additional pressure on the silo industry. Consequently, it becomes increasingly challenging to apply the grading regulations fairly in accordance to the Agricultural Products Standard Act. Grain SA collaborates with the silo industry and DAFF to find a sufficient solution for the execution of the soybean grading regulations. It is of importance that producers take cognisance of grading regulations and to make sure that the grading of their products are done according to the act. It is applicable for all the grain and oilseeds commodities and not only soybeans. Grading of sorghum Cultivars which do not necessarily have to meet malting requirements are increasingly needed by the sorghum industry. The demand increases for cultivars, which do not contain tannins and are also suitable for the milling and bio-ethanol industries, while the demand for sorghum feed (GL cultivars) is almost non-existent. We proposed to the industry to accept changes to the regulation in order to differentiate between tannin free (0<,2%) and tannin containing cultivars. Therefore the GL grade may cease to exist and the remaining GL cultivars that meet the requirements are added to the GM cultivar list. The nature of the deviations in the regulations remains unchanged. The GM grade is applicable with reference to tannin free sorghum while the GH grade refers to tannin-containing sorghum. The proposal still needs to be accepted. Grading of wheat The qualified slackening of the grading regulations and cultivar release criteria for wheat should not have a negative influence on the milling and baking quality of wheat, but could lead to a more just grading system in the market place. Grain SA proposed changes to the grading regulations for the industry’s consideration and are actively engaging with value chain members to reach strategic solutions as a matter of urgency. |

Ten einde marktoegang te verkry, bemark die pas bekendgestelde aanlegte die plaaslik geproduseerde oliekoek teen afslag. Gegewe die krimpende persmarge sal die afslag na verwagting beëindig word sodra die tandekryprobleme van die nuwe sojaboonbrekingskapasiteit voldoende opgelos is. Handel en handelsbeleidomgewing Koringinvoertarief Die Kommissie vir Internasionale Handelsadministrasie (ITAC) het Graan SA se aansoek om ‘n nuwe verwysingsprysvlak van 4 per ton in plaas van 5 per ton op 23 April 2013 goedgekeur. ‘n Koringtarief is vasgestel toe die FOB Golf HRW Nr. 2-koringprys vir drie opeenvolgende weke in September tot ‘n vlak van 4 per ton gedaal het. Hoewel die tarief van R156 per ton nie voldoende is om die produsenteprys vir koring te verhoog nie, maak dit ‘n meer stabiele omgewing en sekerheid moontlik sodat produsente dit kan oorweeg om koringproduksie te verhoog. Liggingsdifferensiale Talle insette is voor en sedert 2008 gemaak om die funksionering van die termynmark en die liggingsdifferensiaal te hanteer. Graan SA het in 2013 en 2014 ‘n beduidende hoeveelheid hulpbronne gebruik om op die afskaffing van die liggingsdifferensiaal te fokus. Toe lede voor die waarskynlikheid te staan kom dat die organisasie daarin kan slaag om die differensiaal vir ‘n proeftydperk van twee jaar te laat afskaf, het sommige die impak van geen differensiaal, heroorweeg. Graan SA het gevolglik teenvoorstelle van ander lede ontvang om die differensiale in plek te laat. Die JSE het ‘n besigheidsbesluit geneem om die differensiaalstelsel te behou, en geredeneer dat die differensiaalstelsel hulle sakemodel ondersteun en dat die besluit in hierdie lig geneem is. Graan SA ondersteun nie die JSE se liggingsdifferensiaalstelsel nie en is van mening dat dit afgeskaf moet word. Hoewel ons nie die differensiaal ondersteun nie, word alles moontlik gedoen om dit so laag as moontlik te hou. Ons gaan dus voort om die billike berekening van die differensiaal deur die JSE te moniteer en bespreek die saak deurlopend met die JSE. Die mieliedifferensiaal het in Maart 2014 gemiddeld met 9,8% gestyg. Dit het ná intense onderhandelinge met die JSE en ‘n oorspronklike voorgestelde styging van 12,9% gevolg. Graan SA het vir produsente meer as R100 miljoen gespaar. Graan SA het verder vir die JSE aangedui dat die mielieliggingsdifferensiaal by Wesselsbron verkeerd gepubliseer is. Die JSE het die gemiddelde spoor- teenoor padaflaaiverhoudings reggestel. Met die bygewerkte verhoudings vir die Wesselsbron-differensiaal wat by berekeninge ingesluit is, word dit op R15 per ton laer as die voorheen gepubliseerde koers herbereken. Dit beteken ‘n potensiële besparing van ongeveer R4,125 miljoen vir produsente wat mielies by die Wesselsbronsilo lewer. Kontantmarkdeursigtigheid en basisverhandeling Prof Mathew Roberts is in 2008 deur die Nasionale Landboubemarkingsraad (NLBR) aangestel om die funksionering van die termynmark te ondersoek. Hy het aangedui dat die differensiaalkwessie ‘n simptoom is van ‘n ander probleem, naamlik om die deursigtigheid van kontantmarkpryse te hanteer. Deursigtigheid ten opsigte van kontantmarkpryse ontbreek in ‘n beduidende mate. Die ontwikkeling van die kontantmark en deursigtigheid moet die fokus wees in ons toekomstige doelwitte om die belangrikheid van die liggingsdifferensiaal in kontantmarktransaksies te verminder. Mnr Arlan Suderman sê dat die deursigtige kontantmark die beste aanwyser van fundamentele vraag en aanbod-elemente in die VSA is. Deursigtigheid is ‘n noodsaaklike komponent van ‘n akkurate kontantmark wat ware fundamentele vraag en aanbod-elemente weerspieël. Sonder daardie deursigtigheid weet produsente nie of die prys wat aangebied word, werklik produksie sal stimuleer, vraag sal verlangsaam, of wat ook al op daardie tydstip nodig is nie. Sonder deursigtigheid kan die eindgebruiker nie weet watter prys hy moet aanbied om voldoende produksie aan te moedig, of in sommige gevalle produksie te ontmoedig nie, aangesien voorrade ‘n las is. Deursigtigheid is gevolglik ‘n kernwaarde wat rolspelers in die VSA na aan die hart lê. Die produsente sowel as die eindverbruikers stamp voortdurend koppe om seker te maak dat ‘n hoë vlak van deursigtigheid op alle vlakke van die kommoditeitsmarkte gehandhaaf word. Hulle werk voortdurend aan nuwe stelsels om vraag en aanbod-data te rapporteer, terwyl kontantpryse wat aangebied en betaal word op alle vlakke van die bemarkingstelsel ook aangemeld word. Mieliebemarkingsjaar Die bemarkingsinligtingjaar vir verslagdoening oor vraag en aanbod vir alle wintergraan strek van Oktober tot September elke jaar. Netso strek die bemarkingsjaar vir somergraan, buiten vir mielies, van Maart tot Februarie. Graan SA het aan die bedryf voorgestel dat die bemarkingsjaar vir mielies ook van Maart tot Februarie moet strek. Die geskatte potensiële vroeë leweringsyfers en die gevolglike skatting van eindvoorraad het die potensiaal om ‘n beduidende impak op die onbestendigheid van markpryse te hê. Die voorgestelde verandering aan die mieliebemarkingsjaar sal help om hierdie probleem te oorkom en voedselsekerheid ondersteun. Geraamde voorraadvlakke aan die einde van die bemarkingsjaar bepaal markpryse gedurende die jaar. Die onseker syfer in die jaarlikse vraag en aanbod-skattings, wat ‘n beduidende gewig in Maart en April het, is die onvoorspelbare vroeë leweringsyfer. Om die bemarkingsjare te verander, beteken dat die vroeë leweringskwessie heeltemal geïgnoreer kan word, en groter voorspelbaarheid en markdeursigtigheid verseker word vir rolspelers soos produsente wat nie die vermoë het om die vroeë leweringsyfer akkuraat te voorspel nie. Die gemiddelde bydrae (oor ‘n tydperk van tien jaar vanaf 2005 tot 2014) van die vroeë leweringsyfer as ‘n persentasie van eindvoorraadvlakke, is 34%, en vir die benuttingsyfer, 31%. Die vroeë leweringsyfer het in 2014 ‘n hoogtepunt van 81% van lewerings as ‘n persentasie van eindvoorraad bereik, en in 2006 ‘n laagtepunt van 3%.Die onsekerheid van vroeë lewerings kan heeltemal uitgeskakel word deur die bemarkingsjaar vir inligtingverslagdoeningsdoeleindes vanaf Mei tot April na Maart tot Februarie te verander. Graan SA se vraag en aanbod-inligting sal hierdie bemarkingstydperk weerspieël. Handelaarstoewydingsverslag Van der Vyfer en Meyer (2014) het in hulle verslag, Positioning reporting by category in agricultural derivatives markets: Should South Africa follow international best practices? gemeld dat dit op die oog af lyk asof Suid-Afrika met internasionale praktyke ooreenstem. Daar is internasionaal ‘n veldtog om regulasies vir kommoditeitsmarkte te verhoog ten einde deursigtigheid te verbeter. Talle ontledings verwys na die rol en belangrikheid van inligting. Volgens die bevindings van hierdie navorsing, wat deur Graan SA geïnisieer is, is die kategorisering van posisies geneem (verskansing of spekulasie) op die JSE se Mark vir Afgeleide Kommoditeite (JSE CDM) onvermydelik, veral as die CDM met internasionale praktyke wil ooreenstem. Daar moet egter beklemtoon word dat likiditeit op die CDM nie vir dieselfde gedetailleerde verslae voorsiening maak nie, en aanvanklik sal dit waarskynlik totale op ‘n hoë vlak verskaf. Dit kan egter ‘n begin wees. Sonder hierdie data (oor tyd) en die ontleding wat daarop volg, kan plaaslike beleidmakers potensieel weer die volgende finansiële ineenstorting en dus die bedreiging vir voedselsekerheid vermy deur hoë kommoditeitspryse, maar ook produksie deur lae pryse wanneer die korrekte prysseine nie by die produsente uitkom nie. Internasionale handel Die langdurige Ekonomiese Vennootskapsooreenkoms(EPA) onderhandelinge tussen ‘n groep Suider-Afrikaanse Ontwikkelingsgemeenskap (SAOG)-lande (Angola, Botswana, Lesotho, Mosambiek, Namibië, Suid-Afrika en Swaziland) en die EU is uiteindelik op 15 Julie 2014 afgehandel. Graan SA het dit reggekry om ‘n beperkte tariefkwota van 300 000 ton op ingevoerde koring te beding. Voorkeur in Suid-Afrika sal tussen 1 November en 31 Januarie geld, en in Namibië tussen 1 Desember en 28 Februarie. Vir Suid-Afrika en Namibië kan koring as deel van hierdie kwota in die toekoms slegs deur Durban, Richardsbaai en Walvisbaai versend word. Graderingsregulasies Gradering van sojabone Die vinnige uitbreiding van sojaboonproduksie plaas bykomende druk op die silobedryf.Dit word gevolglik toenemend uitdagend om die graderingsregulasies billik in ooreenstemming met die Wet op Landbouprodukstandaarde toe te pas.Graan SA werk met die silobedryf en die DLBV saam om ‘n bevredigende oplossing vir die uitvoering van die sojaboongraderingsregulasies te vind.Dit is belangrik dat produsente kennis moet neem van die graderingsregulasies en seker moet maak dat die gradering van hulle produkte in ooreenstemming met die wet gedoen word.Dit is van toepassing op al die graan- en oliesaadkommoditeite, en nie net op sojabone nie. Gradering van sorghum Kultivars wat nie noodwendig aan die moutvereistes hoef te voldoen nie, word toenemend in die sorghumbedryf benodig. Die vraag na kultivars wat nie tannien bevat nie, neem toe, en dit is ook geskik vir die maal- en bio-etanolbedryf, terwyl die vraag na sorghumvoer (GL-kultivars) feitlik niks is nie. Ons het aan die bedryf voorgestel dat veranderinge aan die regulasie aanvaar word om tussen tannienvrye (0<,2%) en tannienbevattende kultivars te onderskei. Die GL-graad kan dus dalk verdwyn en die oorblywende GL-kultivars wat aan die vereistes voldoen, sal by die GM-kultivarlys gevoeg word. Die aard van die afwykings in die regulasies bly onveranderd. Die GM-graad is van toepassing ten opsigte van tannienvrye sorghum, terwyl die GH-graad verwys na sorghum wat tannien bevat. Die voorstel moet nog aanvaar word. Gradering van koring Die gekwalifiseerde verslapping van die graderingsregulasies en kultivarvrystellingskriteria vir koring behoort nie ‘n negatiewe invloed op die maal- en bakgehalte van koring te hê nie, maar kan tot ‘n regverdiger graderingstelsel in die mark lei. Graan SA het veranderinge aan die graderingsregulasies vir die bedryf voorgestel en gesels aktief met waardekettinglede om dringend strategiese oplossings te kry. |

|

Publication: December 2014

Section: Industry Services