- Follow us:

- Our Commodities:

-

December 2013

ERNST JANOVSKY, HEAD: AGRIBUSINESS, ABSA

The livestock feed industry is a major consumer of grain and oilseeds. Without a profit expectation for this industry, the consumption of livestock feed will decline and that will be negative for grain and oilseeds producers.

Profit is derived from the product prices as well as the cost of production. Let us investigate the expectations of the major livestock enterprises.

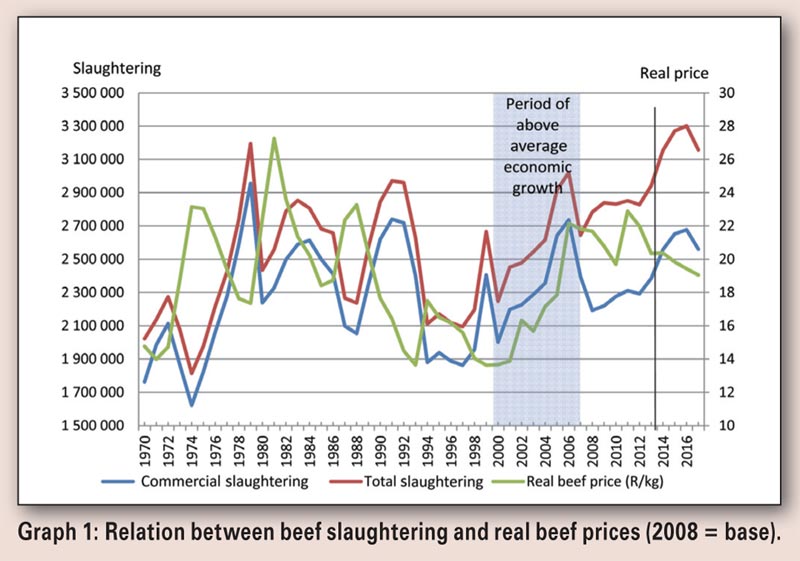

Beef

The good old times where real beef prices increased in spite of an increase in slaughtering, is something of the past and we are once again back to normal. There has always been a strong correlation between beef slaughtering and real beef prices – as slaughtering increased, real beef prices declined. However, during the period of 2000 to 2006, as a result of good international economic growth as well as domestic economic growth, real beef prices increased in spite of an increase in slaughtering.

Since then, we experienced the world financial crisis and in South Africa a slowdown in economic growth which implies that consumers are taking strain. The net effect is that as spending continued to increase, real beef prices continued to decline.

The future however does not look as rosy, as far above average production conditions over the past five years created some leeway in a sense that producers did not need to slaughter their cattle as there was enough fodder available to carry stock over. All of this however changed dramatically during the past season given the first indicative drought in the western areas of the country, this combined with a severe dry year in Namibia and one of the biggest herds we have ever had in South Africa, has led to a sharp increase in slaughtering.

An above average rain season can bring some relief, but given the long-term prediction, it is expected that we are moving into a dryer rainfall cycle. We therefore expect slaughtering to increase as producers start to cut back on production and we also expect that the national beef herd will be under pressure and start to shrink.

As communal areas’ contribution to total slaughtering has increased substantially over the past years, it is expected that given the level of fodder management, communal producers would be much more vulnerable to the effects of a drought than commercial producers as they do not have any reserves whether financial or in the form of fodder.

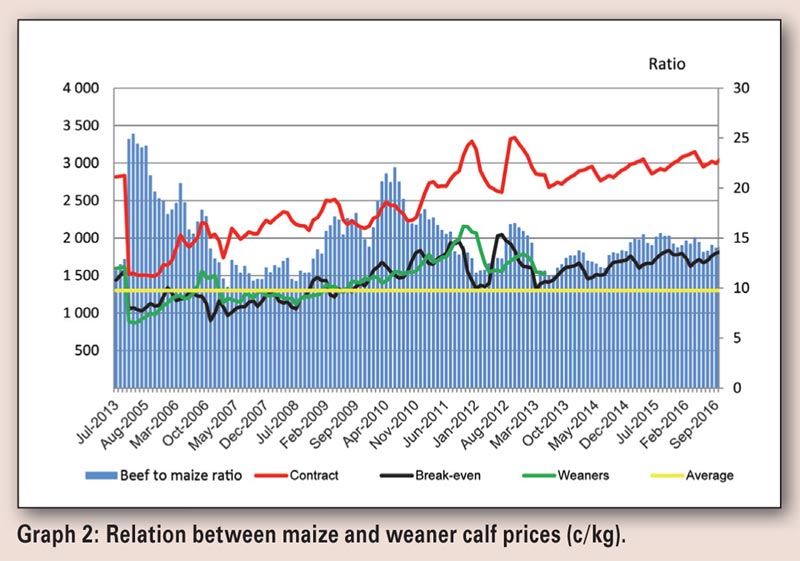

Lower world commodity prices for coarse grains lead to a lowering of feed prices, unfortunately this was to some extend set off by a weaker rand/dollar exchange rate. Intensive livestock industries, such as feedlots, therefore continue to take some strain.

Beef outlook

Slaughtering is expected to continue to increase over the next few years placing downward pressure on producer prices as demand is expected to remain fairly flat. Class A2 beef prices are expected to decline from the anticipated R31/kg in December, to just below R27/kg in May 2014.

Weaner calf prices are expected to show some recovery, but will struggle to exceed R18,50/kg in live weight in 2014.

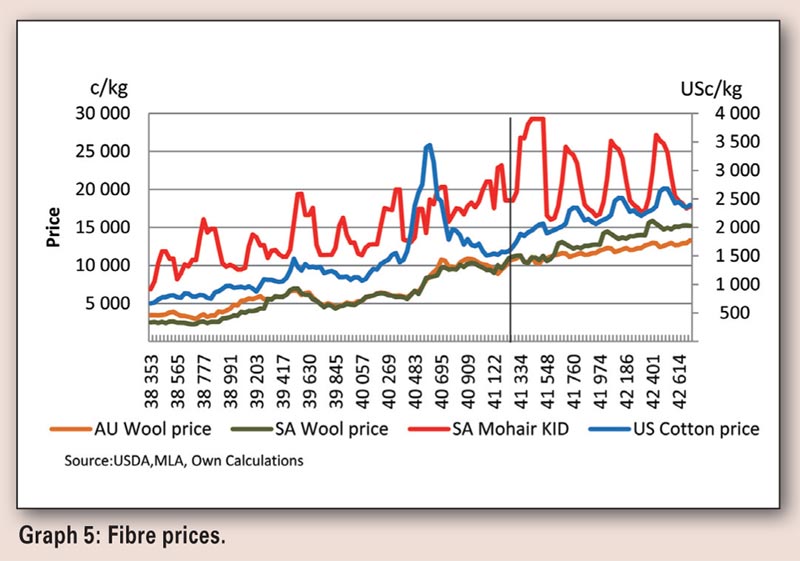

Mutton

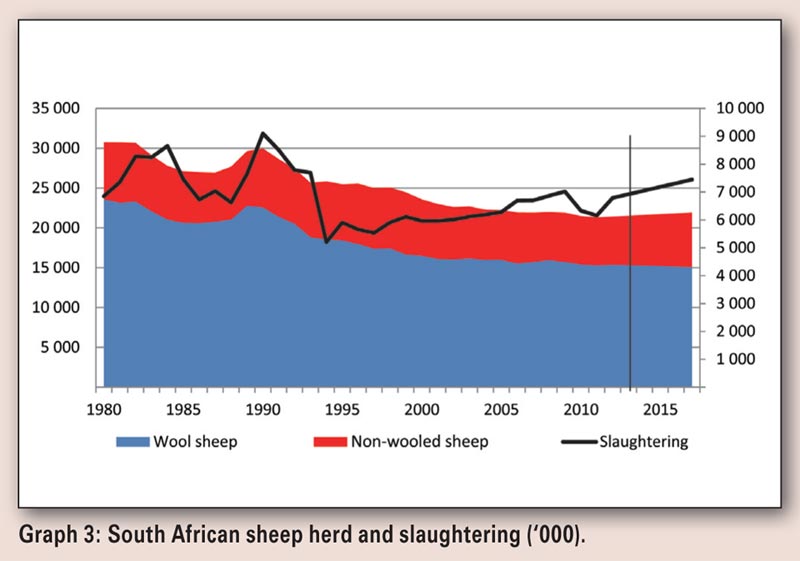

World sheep numbers continue to decline; this is mainly due to the dry production conditions in Australia triggering herd liquidation, with a resulting decline in world mutton production.

On the domestic front the national sheep is showing some recovery nationally after reaching a low during 2010 which coincide with the outbreak of Rift Valley fever which led to a decline of almost 30% in mutton production. Due to the decline in production, prices peaked at a new all-time record of R54,55/kg for Class A2 in August 2011.

Production recovered to pre-2011 prices during the 2012 season, with the bulk of the producers now inoculating against Rift Valley fever. Herd numbers have also shown some recovery as producers muster the art of keeping their flocks safe from vermin and stock theft.

Mutton and wool production is expected to continue to increase with the help of higher mutton and wool prices.

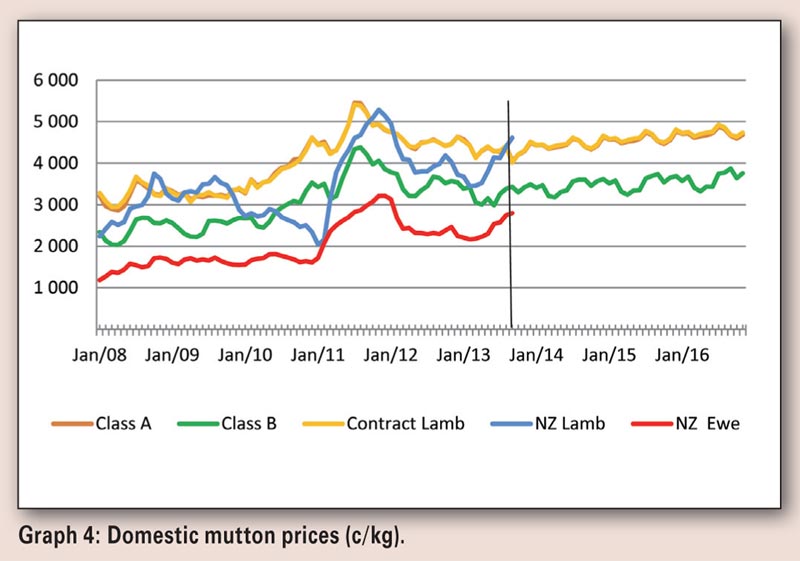

Import parity prices for lamb and mutton improved substantially on the back of a weaker exchange rate as well as slightly higher international prices due to the easing of the drought in Australia, bringing some relief with regards to forced herd liquidation.

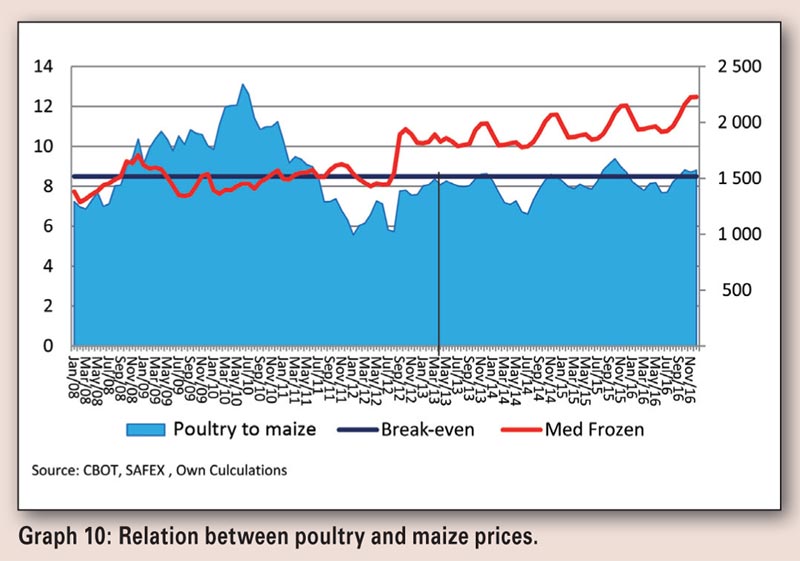

Imported lamb prices are currently trading above local lamb prices and imports are limited to live imports from our neighbouring states, with the potential to create some opportunity for prices to increase. High volumes of beef, pork and poultry however continue to place mutton prices under pressure. Mutton to maize price ratios however remains very favourable hence the good demand for feeder lambs for the feedlots.

Mutton outlook

Mutton prices are expected to slide lower as seasonal production volumes increase with prices even trading below R40/kg with some relief towards December. As mutton is positioned as an elite product and consumers are still in trouble, it is expected that prices will continue to remain under pressure with only inflationary price increases over the next few years. Wool production is expected to continue to grow in spite of a decline in the wool bearing sheep herd, this is mainly the result of higher wool prices as well as improvements in technology and genetics.

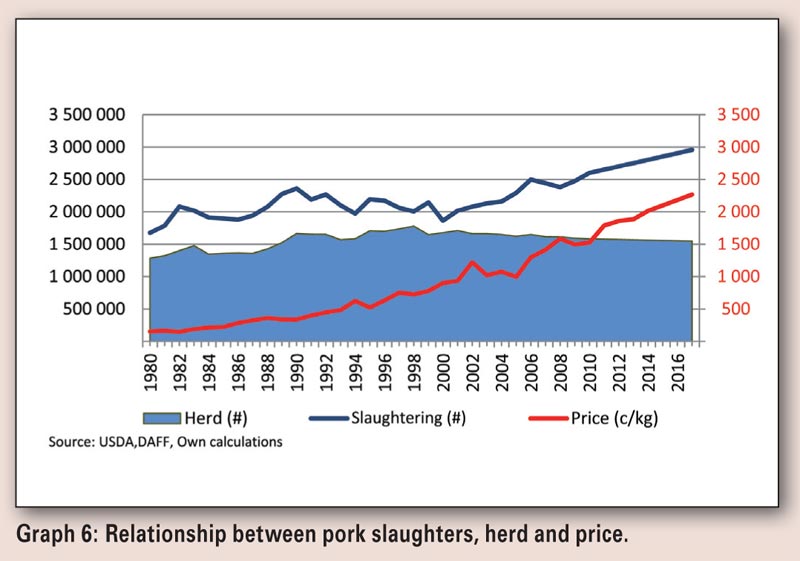

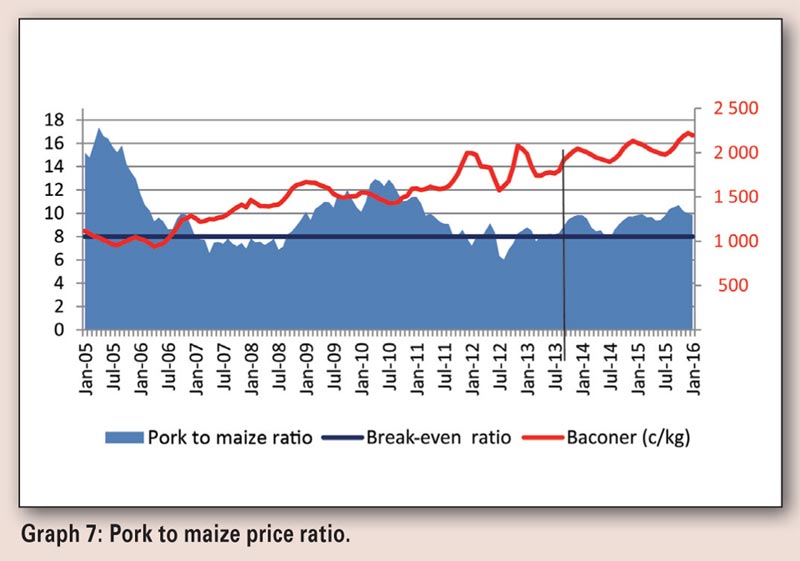

Pork

World pork production continues to increase in spite of relatively high international grain prices. World pork consumption still tops that of poultry, but poultry is gaining and should exceed pork production in the next few years.

Domestic pig herds continue to decline with a further acceleration over the last year as unfavourable production conditions continue to squeeze marginal producers out of the industry. In spite of a decline in pig herd numbers, slaughtering continue to grow – this is mainly due to the implementation of new technology in terms of all-in-all-out housing and climate control, as well as genetics. As a matter of fact, pork has become so lean that there is a shortage of fat in the world for the production of soap and other by-products.

Over the past year, negative pork to maize price ratios placed production margins under pressure with a resulting exodus of the bulk of the backyard and swill pork producers.

This has led to a shortage of pork in the market over the last weeks and a resulting increase in price. The stronger price was further underpinned by an increase in poultry import parity prices. Thanks to lower international grain prices, domestic feed prices softened in spite of a weaker exchange rate, this combined with new production technology as well as improvements in technology led to an increase in production margins. It is therefore expected that production will continue to increase and that further expansions in the industry by some of the more efficient producers, can be expected.

The weaker rand has also pushed import and export parity prices higher and it is currently quite feasible to export pork at good margins.

Pork outlook

Pork prices are expected to remain fairly stable during 2014, this combined with lower feed prices due to lower international commodity prices, will lead to production expansion under the more efficient pork producers.

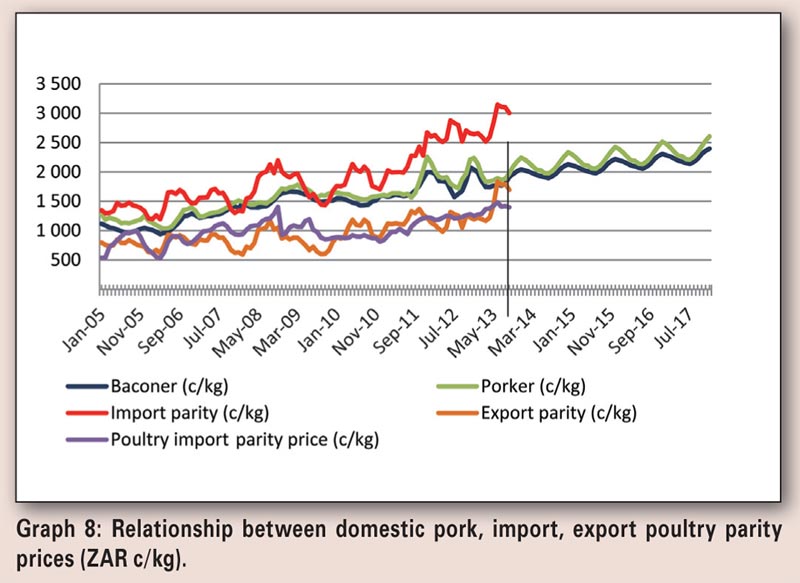

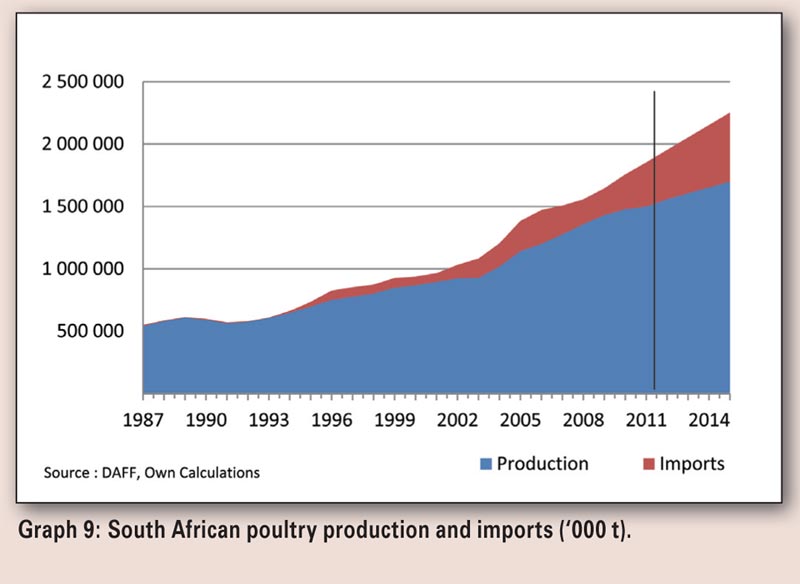

Poultry

Poultry production shows the first signs of retraction; this is mainly due to an increase in production cost with a resulting squeeze on production margins. This combined with very low import parity prices and an increase in imports, continued to place pressure on the industry as producers are unable to pass on higher production costs to consumers due to imports.

Production margins have improved slightly over the past six months due to lower international grain prices; however this is not enough to compensate for the price increase which is needed to sustain profit margins.

With the announcement of an increase in import tariffs, there is some relief for producers. This will however only impact imports of ± 40% – with 60% of the imports still being imported into South Africa from Europe under a free trade agreement. It is therefore expected that production margins will remain under pressure with a further potential downscaling on production.

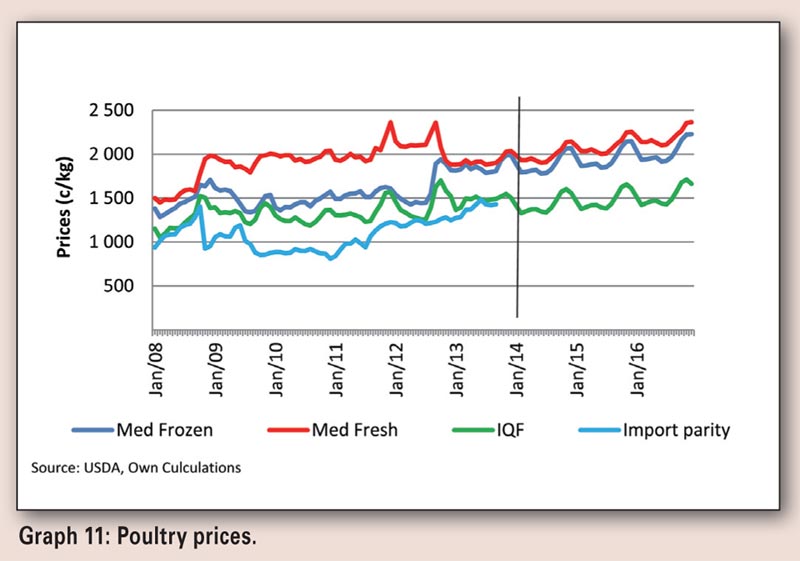

This is especially true should the exchange rate continue to strengthen. Poultry prices are therefore expected to continue to move sideways with very little upward potential. The industry has however cleaned up its act and lowered the amount of water that is injected into the frozen product, hence the increase in price of whole frozen birds. However to be able to compete against the very cheap individually quick frozen product (IQF), they still need to lower brine injection percentages.

Poultry outlook

It is expected that domestic poultry production will continue to decline as production margins remain under pressure. Prices will also tend to move sideways due to competition from imports which are further impacted by a stronger rand.

The net impact for the livestock industry on grain is fairly neutral with poultry consumption expected to decline and beef, mutton and pork production pricing up some of the slack.

Publication: December 2013

Section: Input Overview