- Follow us:

- Our Commodities:

-

June 2025

| YOLANDI MARAIS, AGRICULTURAL ADVISOR, DUNAMUS |

|

RUNNING A FARMING BUSINESS CAN BE VERY REWARDING – SEEING YOUR PRODUCE GROW, REACHING MATURITY, AND SELLING IT TO REALISE AN INCOME AND GENERATE PROFITS. AT THE SAME TIME, IT CAN BE VERY DAUNTING BECAUSE SO MANY THINGS CAN GO WRONG. YOUR CROP CAN BE AFFECTED BY TOO LITTLE OR TOO MUCH RAIN, HAIL, EARLY FROST, PESTS AND DISEASES.

Farming is a risky business, but farmers who manage these risks well can enjoy the rewards of profitable, resilient farming businesses.

Being resilient means that the farming business can experience setbacks, such as natural disasters or crop failures, without the setbacks forcing the farm to shut down. Being resilient means that you, as the farmer and the business, can make a come-back from the setback and continue farming. So, how do you build a resilient farming business that can endure the risks?

UNDERSTAND YOUR FARM’S COST STRUCTURE

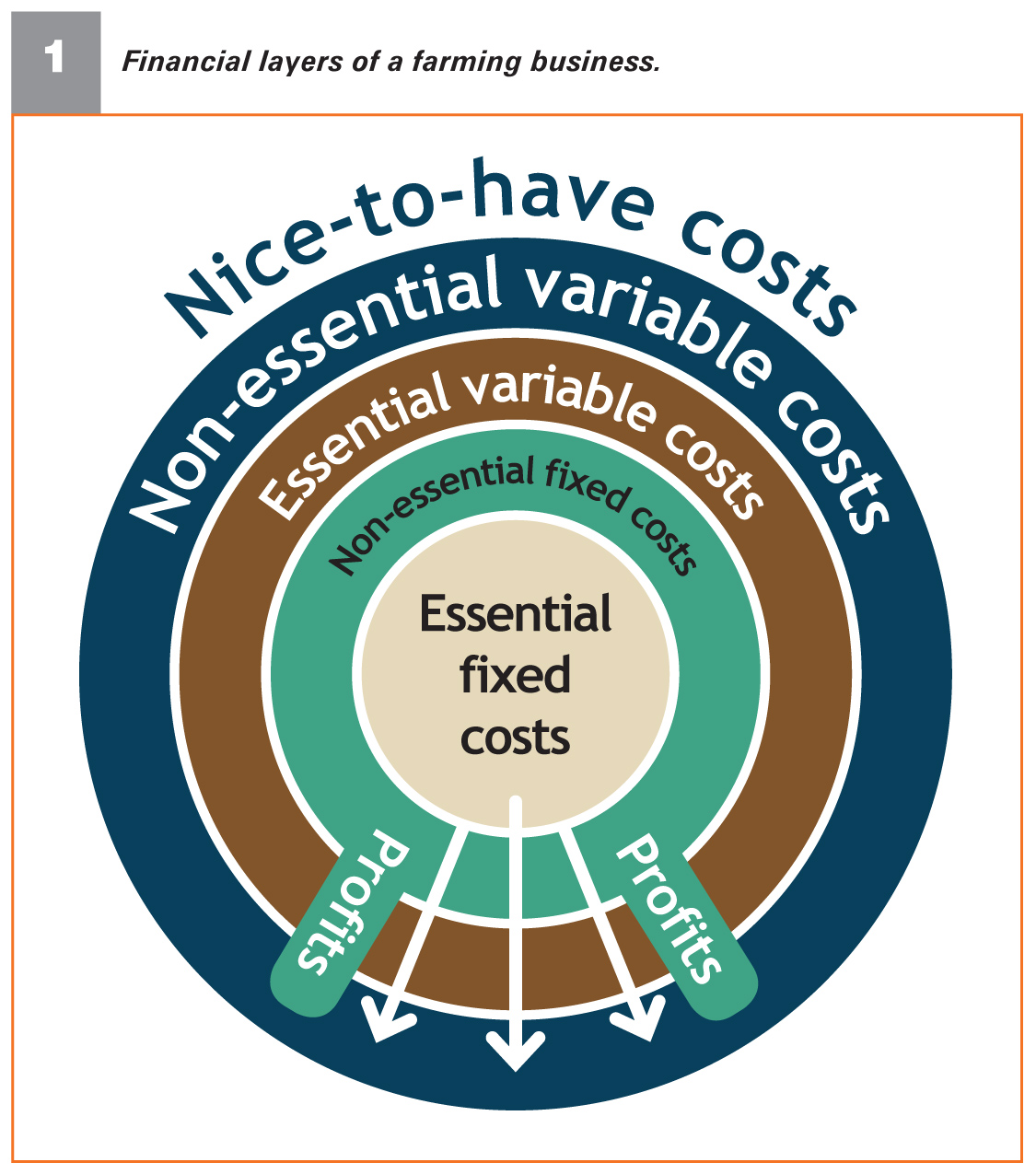

Not all expenses/costs on a farm are essential. Everyone would like to believe that all costs are necessary, but if you critically evaluate them, they can be divided into different layers as illustrated in Figure 1.

The different layers of a farming business can be explained as follows:

The different layers of a farming business can be explained as follows:

Essential fixed costs

These costs are absolutely necessary to keep the business functional and include land rent, bank fees, electricity (line fees), permanent salaries and wages and vehicle licences.

Non-essential fixed costs

Non-essential fixed costs are also fixed over the short term but are not as essential as the essential fixed costs. Examples include farmers’ drawings for living costs, extensive short-term insurance, large fixed contracts for telephone and Internet, and subscriptions.

Essential variable costs

Variable costs are costs that vary as production varies, which means that if you do not produce anything, these costs should be zero. Examples are seed, fertiliser, chemicals and fuel. The more hectares you plant, the higher these costs will be. One cannot produce crops without the essential variable costs like seed, fertiliser and chemicals.

Non-essential variable costs

These costs also vary as production varies, but are non-essential, meaning that is not necessary to produce a crop or raise cattle. Examples are extra minerals or vitamins (for livestock), immune boosters, soil health add-ons like micro-elements and extra casual labour to help on the farm. These costs can positively impact production but are not an essential element.

‘Nice-to-have’ costs

As the heading explains, these costs are ‘nice-to-have’ on the farm but are not essential for the farming business to operate. Most of these costs can make the farmer’s life easier or contribute to the farm’s image, such as new fences and gates, upgrading farming vehicles, tractors or machinery, gadgets, technology and home renovations.

All of a farm’s costs must be covered by either its income or its profits. Remember, the income is the total income you generate from sales, whereas the profits are the funds that remain after the costs have been covered. Essential costs must be covered by the income, whereas the non-essential and ‘nice-to-have’ costs should be covered by the profit.

KEEP THE COSTS LEAN

To ‘keep costs lean’ means to reduce unnecessary expenses. When you understand the cost structure and different financial layers of the business, try to keep the circles as small as possible.

Make a distinction between the essential and non-essential costs and keep the non-essential costs to a minimum. The higher the costs, the wider the circles (Figure 1). It becomes increasingly difficult to cover the costs as the income and profits are diminished.

When a farmer can limit the costs without negatively impacting yields or production, the profit will be higher. This provides an opportunity to buy the non-essential items or reinvest them back into the farm.

Keeping costs low is part of risk management to ensure your business is resilient and will withstand tough times. It is wiser to spend money in your hand than to spend an expected income that has not realised yet.

Here are some examples to keep the costs low:

REACT FAST

When things go wrong on a farm, it usually happens at a fast rate. If disaster strikes, you must react quickly to the changing circumstances. Do not wait too long to react, as a delayed reaction can be a costly mistake, resulting in less resilience and ability to recover from external shocks.

Farming is a risky but rewarding business. Build a resilient business and keep the cost circles small so that you can enjoy the reaping of a harvest year after year.

Publication: June 2025

Section: Pula/Imvula