- Follow us:

- Our Commodities:

-

September 2020

| Jenny Mathews, Pula Imvula contributor. Send an email to jennymathews@grainsa.co.za |

|

The diesel rebate is basically a diesel refund system. It is a tax relief made available for various activities in the farming, mining and forestry sectors among others.

The intention is to lighten the burden carried by local industries that must compete in the international sector where for e.g. many farmers receive subsidies and other forms of protection. It is also intended as a relief offered on vehicles that do not necessarily utilise the public roads networks since they primarily work in designated areas, for example on farms. The Diesel Refund Scheme is currently administered through the VAT system in terms of the Customs and Excise Act.

This rebate provides full or partial relief from the General Fuel Levy and the Road Accident Fund levy. As of 1 April 2020, the General Fuel Levy increased to 355 cents per litre; and the Road Accident Fund levy increased to 207 cents per litre.

A farmer qualifies for a rebate on 80% of his lawful use in terms of the qualifying litres. This would be litres used for the primary farming activities and would exclude diesel consumed for personal and private use. Farming enterprises are entitled to a diesel rebate in respect of diesel that is physically delivered to the premises of the farm of a qualifying user. Many farmers have been claiming the rebate even when diesel is purchased at other outlets for farming activities. However, a Supreme Court of Appeal judgement made in November 2019 provided guidance on the Act, finding that a qualifying taxpayer may only claim a rebate for the diesel fuel stored and used on its own premises.

HOW DO I QUALIFY FOR A REBATE?

In order to qualify for a diesel rebate:

GENERAL

It is important for farmers to understand that the diesel rebate is a special concession being made. SARS officials are always looking out for those who are abusing the system and using it fraudulently. It is to the benefit of the broader farming sector that we respect the legislation and keep our slate clean and honourable.

The diesel rebate is one of the only benefits farmers receive from the government so we should strive to keep records that are beyond suspicion. At the same time, should farmers experience frustration and problems with the diesel rebate system and the implementation thereof, Grain SA can be of assistance and farmers should feel free to contact the head office as long as they can provide accurate records and their reasons for the frustration.

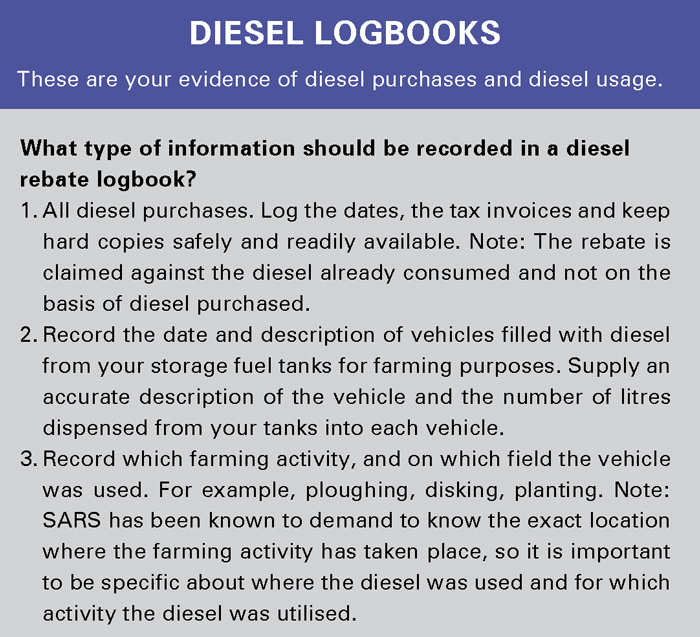

An example of a diesel usage logbook can be found on the SARS website at:

https://www.sars.gov.za/AllDocs/LegalDoclib/Drafts/LAPD-LPrep-Draft-2013-17%20-%20Draft%20Tariff%20Amendment%20Diesel%20Usage%20Logbook.pdf

Publication: September 2020

Section: Pula/Imvula