- Follow us:

- Our Commodities:

-

September 2021

| RICHARD MCPHERSON, AGRIBUSINESS AND PROJECT MANAGEMENT CONSULTANT |

|

The results of the summer maize crop planted in 2020 and harvested from June to July 2021 can now be assessed. The actual yields achieved and costs incurred will indicate whether or not there was success achieved within the past season’s operational planning and correct application of the planned inputs.

Producers sold their maize for around R3 200 per ton net in pocket value with many realising a higher than average yield. This is an unusual season in that a national high yield was coupled with a relatively high price.

Lessons for improvement of both efficiency in preparing the lands, planting, growing and harvesting the crop will lead to better assumptions in your budget for the current crop. These calculations should be finalised, at the latest by the end of September, so that the required inputs for maize and other cash crops to be planted can be ordered and the funding all the crops put in place.

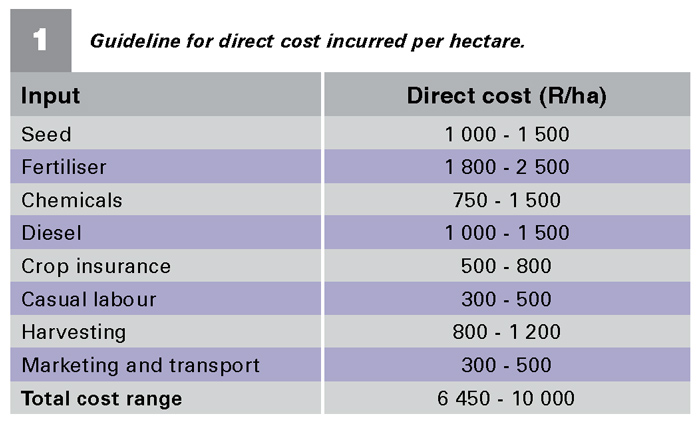

DIRECT COSTS – IMPORTANT FOCUS POINTS

Depending on the accounting conventions used the critical costs included should be for seed, fertiliser including that placed at planting and side-dressed insecticides and herbicides under chemicals, diesel, crop insurance, seasonal labour, harvesting, marketing and transport.

Excluded are consultancy fees, salaries for permanent staff, repairs and maintenance and interest on the total direct input costs. These can be put under fixed costs or overheads.

The total income less the direct costs gives you the amount of financial benefit or ‘gross margin’ derived by the planting of any crop. The positive benefit derived will pay for the fixed costs including permanent staff, repairs and maintenance, interest, capital on long term loans, any other overheads and most importantly the return for labour and money used back to the farmer. Any money left over and above the direct and fixed costs, including the drawings by the farmer and family, would represent the real or net profit for the enterprise.

The objective to generate the sometimes elusive, net or real profit should be calculated and monitored by using a proper accounting programme. The budgets for all operations within enterprises should be set out on interactive spreadsheets for planning and then actual expenses also captured. This is all required for VAT claims or payments, and specific tax returns required. It is recommended that you employ an accounting person or firm to keep this information up to date if you are unable to do it yourself.

ESTIMATED RANGE OF COSTS

It is recommended that proper quotes be obtained from trusted and established suppliers for each of the input costs. If several suppliers for each are approached the conversations involved for the different the physical recommendations made will point to a general consensus on the inputs required for your soil potential and targeted yields. The budget for a dryland crop of 4,5 t/ha will be much less than one of 8 t/ha.

The range for each direct cost incurred per hectare, depending on potential and targeted yield, is shown as a guideline in Table 1. Use your own accurate total to work out both cost per hectare and cost per ton of estimated yield.

CONCLUSION

Work out very carefully, your input cost budget using your actual production history and soil potential keeping a conservative long-term yield potential in mind.

Publication: September 2021

Section: Pula/Imvula