- Follow us:

- Our Commodities:

-

March 2014

PETRU FOURIE, economist: Industry Services, Grain SA

Bread is an important staple food in South Africa and plays an integral role to ensure national food security. Consumers for the most part do not buy food directly from producers and the price consumers pay (real retail value) for food is exceedingly higher than what producers receive (real farm value) for the raw commodity.

The focus of this article is to highlight the small share the wheat producer contributes to the price of a loaf of white bread sold at a retail store. The wheat producer’s share in the retail price of white bread will be examined to demystify a common misconception that producers are responsible for the increases in bread prices. The data in the article is calculated for the last six years to give a proper overview of a wheat producer’s actual contribution.

Background on the wheat price

The price of wheat for a South African buyer is normally determined by the international wheat price, the exchange rate and the local supply and demand for wheat. South Africa is not self-sufficient in the production of wheat and therefore approximately 50% of its local consumption is imported.

South Africa’s dependency on imported wheat increased over time and hence the domestic price for wheat, as reported by Safex, tends to be close to import parity. These imports contribute to higher bread prices than would be the case if all South African demand could be locally produced.

How much wheat in a loaf of white bread?

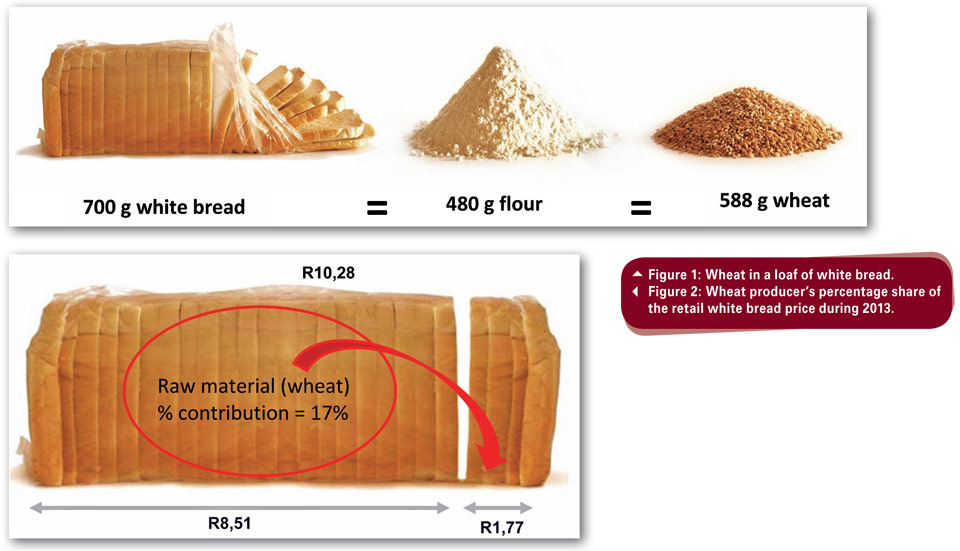

In order to calculate the difference between the real farm value and the real retail value, the following assumptions were made – to bake a 700 g loaf of white bread, an average of 480 g of flour is needed. Again, in order to mill that 480 g of flour, 588 g of wheat is required (Figure 1). Thus, approximately 1 700 loaves of white bread can be produced from 1 ton of wheat.

The price consumers pay for bread versus the price producers receive for wheat

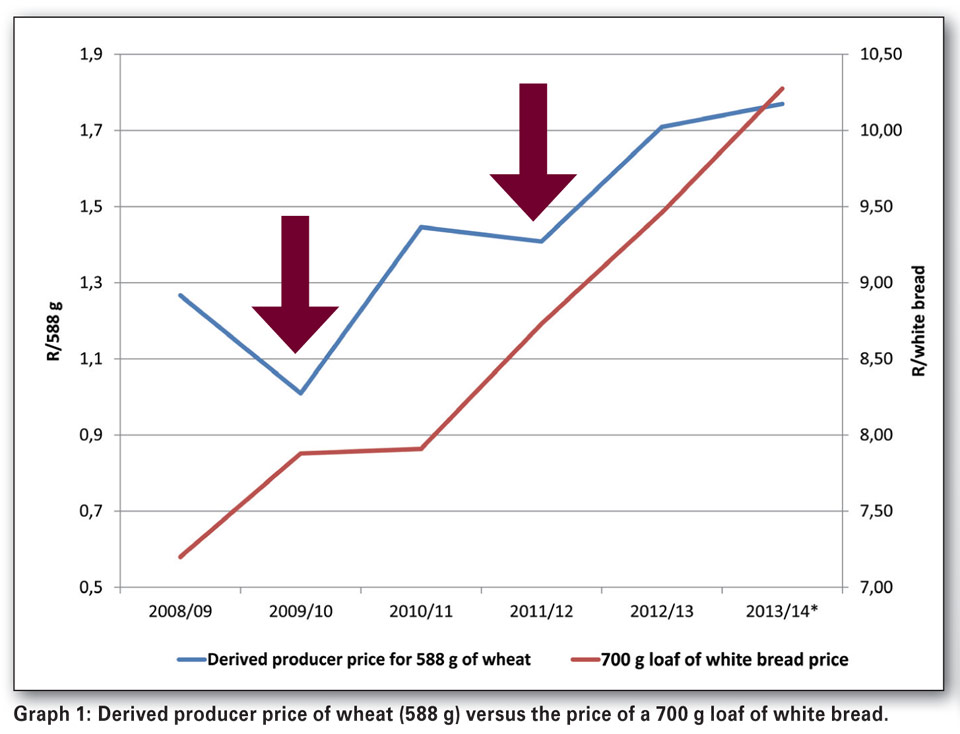

The Western Cape plays a very important role in the supply of wheat in South Africa, accounting for between 35% - 40% of total domestic production. For this reason, the calculations depicted in Graph 1 are based on a derived producer price of wheat for a Western Cape producer in order to produce the required 588 g of wheat for one loaf of white bread.

The derived producer price is determined by calculating the average annual Safex price for each marketing year and deducting the relevant costs, such as the location differential as well as handling and storage costs for grade B2 wheat.

Graph 1 compares the derived producer price of wheat for 588 g of wheat against the annual average price of a 700 g loaf of white bread in a retail store. During this six year period, wheat producer prices declined twice, while bread prices continued to increase, indicating that producers did not fully share in higher retail prices. This is particularly true for the 2009 season, where the producer price of wheat (588 g) decreased from R1,27 in 2008 to R1,01 in 2009 (down 20%), while the price of a 700 g loaf of white bread increased by 9% from R7,20 to R7,88 over the same period.

The same happened during 2011 where producer prices decreased by 3%, while the bread price increased by 10%. Graph 1 clearly shows the widening gap between wheat and bread prices, and that producer price increases were in many cases not responsible for the increase in the bread price to consumers.

Wheat producer’s percentage share of retail white bread price

While input prices increased both for producers and retailers, the producer’s share of the consumer’s rand remained stationary or decreased. Between 2008 and 2013, a wheat producer’s share of a 700 g loaf of white bread fluctuated between 13% and 18%. Figure 2 clearly shows a wheat producer’s percentage share of a retail white bread price (2013).

This indicates that when a consumer bought a loaf of white bread, the raw material (wheat) simply costs R1,77 in comparison to the total bread loaf price of R10,28. For example, if the loaf consists out of 21 slices, the producer’s cost for that bread is only 3,5 slices, while the rest of the wheat-to-bread value chain is responsible for the additional cost.

Costs involved in producing 588 g of wheat

Costs at primary level (i.e. at the level of wheat production) have increased continually due to increases in input costs. This places pressure on producers’ profitability and hence the ability to bring additional hectares into production. Wheat producers are price takers, and in a competitive market, they cannot simply pass their higher costs on to consumers. To date, rising costs have largely been absorbed by producers, often with significant financial loss.

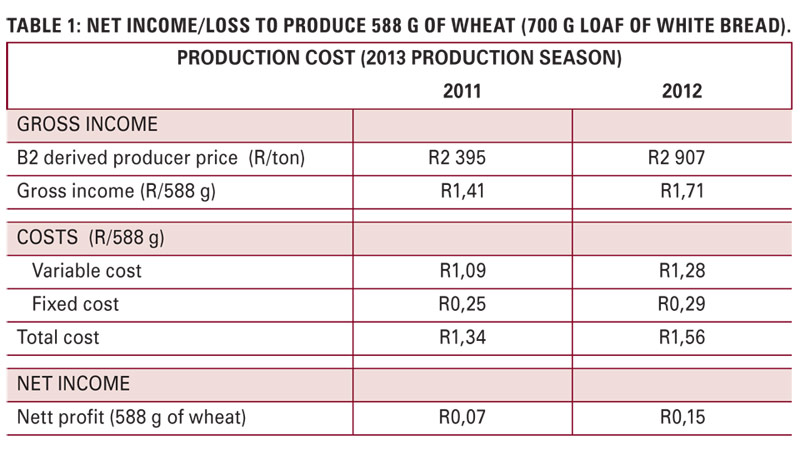

Table 1 shows the gross income, total cost and net income of a Western Cape wheat producer in order to have produced 588 g (700 g loaf of white bread) of wheat during 2011 and 2012. Actual production cost figures were used for calculation purposes.

Over the two year period, the gross income producers received for the 588 g, increased with 30 cents from R1,41 in 2011 to R1,71 in 2012, while the total costs (variable and fixed cost) to produce that same 588 g, increased with 22 cents from R1,34 to R1,56 over the same time period.

The net farming income increased from 2011 to 2012; from making a 7 cent profit in 2011 to making a 15 cent profit in 2012.

Conclusion

Consumers must be sensitised on the pricing of bread and that the increase is not necessarily linked to the producer, but more to the other role-players within the wheat-to-bread value chain.

It is of concern to note the stationary or decreasing share producers get out of the consumer rand and that a wheat producer’s share of a 700 g loaf of white bread fluctuated only between 13% and 18% in the last six years. In some cases the wheat producer even subsidised the consumer.

Publication: March 2014

Section: Other Articles