122 / 138

122 / 138

118

Depreciation of an asset commences when the asset is available for use as intended by man-

agement. Depreciation is charged to write off the asset’s carrying amount over its estimated

useful life to its estimated residual value, using a method that best reflects the pattern in which

the asset’s economic benefits are consumed by the organisation.

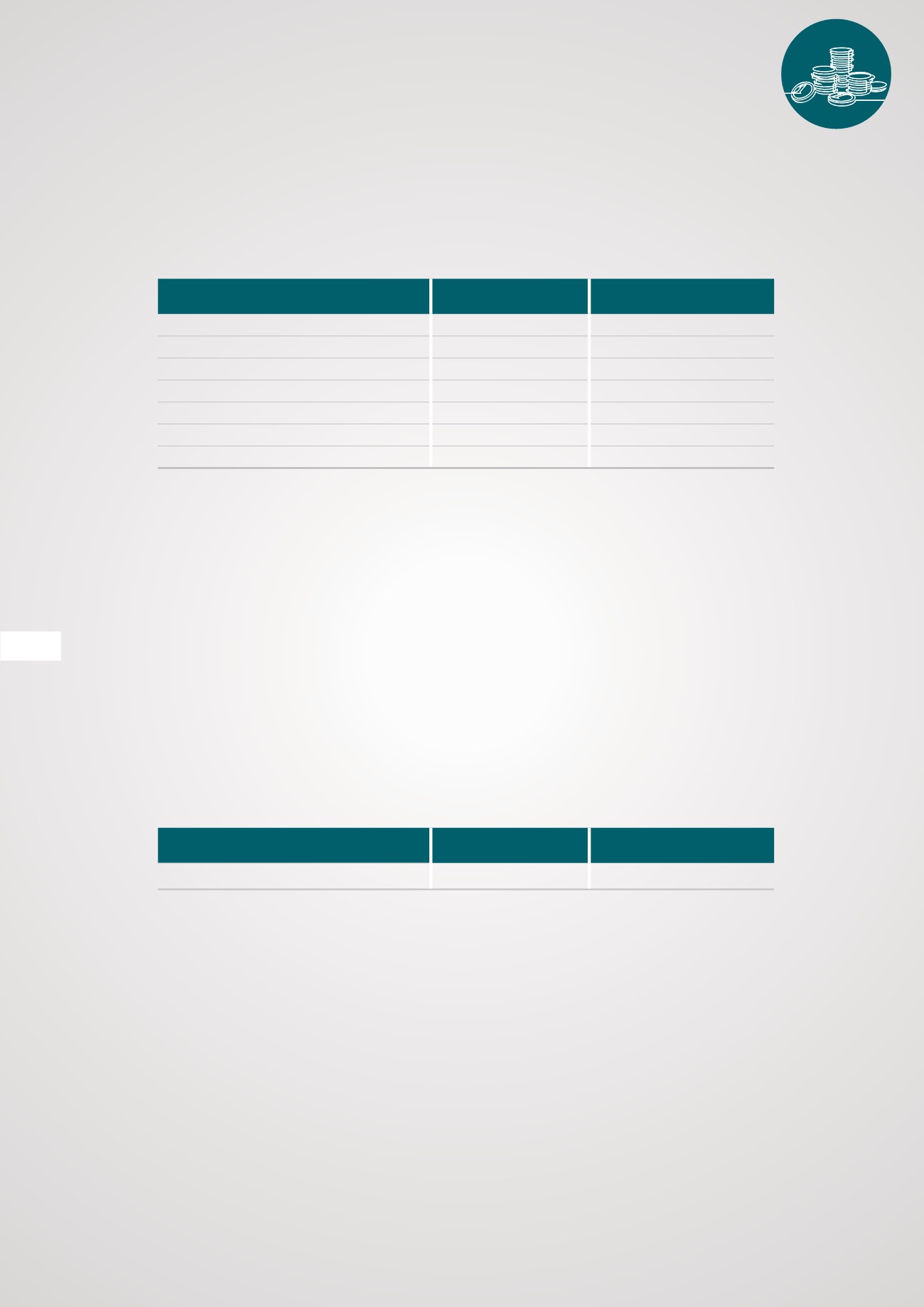

The useful lives of items of property, plant and equipment have been assessed as follows:

ITEM

AVERAGE USEFUL LIFE DEPRECIATION METHOD

Land and buildings

0 - 10%

Straight line

Plant and equipment

20%

Straight line

Motor vehicles

20%

Straight line

Furniture and fittings

20%

Straight line

Catering and other equipment

20%

Straight line

Office equipment

20%

Straight line

IT equipment

20%

Straight line

When indicators are present that the useful life and residual values of items of property, plant

and equipment have changed since the most recent annual reporting date, they are reassessed.

Any changes are accounted for prospectively as a change in accounting estimate.

Impairment tests are performed on property, plant and equipment when there is an indicator that

they may be impaired. When the carrying amount of an item of property, plant and equipment is

assessed to be higher than the estimated recoverable amount, an impairment loss is recognised

immediately in profit or loss to bring the carrying amount in line with the recoverable amount.

An item of property, plant and equipment is derecognised upon disposal or when no future eco-

nomic benefits are expected from its continued use or disposal. Any gain or loss arising from the

derecognition of an item of property, plant and equipment, determined as the difference between

the net disposable proceeds, if any, and the carrying amount of the item, is included in profit or

loss when the item is derecognised.

2.6 INTANGIBLE ASSETS

Intangible assets have a finite useful life and are carried at cost less accumulated amortisation and any

accumulated impairment losses. Amortisation is calculated using the straight-line method to allocate

the cost of intangible assets over their estimated useful lives as follows:

ITEM

AVERAGE USEFUL LIFE DEPRECIATION METHOD

Computer software

33%

Straight line

2.7 FINANCIAL INSTRUMENTS

Initial measurement

Financial instruments are initially measured at the transaction price (including transaction costs

except in the initial measurement of financial assets and liabilities that are measured at fair value

through profit or loss) unless the arrangement constitutes, in effect, a financing transaction, in which

case it is measured at the present value of the future payments, discounted at a market rate of

interest for a similar debt instrument.

Financial instruments at amortised cost

These include trust funds, cash and cash equivalents, trade and other receivables and trade

and other payables. Those debt instruments which meet the criteria in section 11.8(b) of the

standard are subsequently measured at amortised cost using the effective interest method.

Debt instruments which are classified as current assets or current liabilities are measured at the

undiscounted amount of the cash expected to be received or paid, unless the arrangement

effectively constitutes a financing transaction.

FINANC

IAL

STATEMEN

TS

Basi

s of

p

re

parati

on and

sum

mary of significant

acco

unting

pol

icie

s (conti

nued

)